Evan Armstrong was a lead writer at Every who explored profit and power in technology in Napkin Math.

The Impossibility of Being Charlie

RIP to nerd Jesus

Dec 7, 2023 · 10 min readUpdated Jul 10, 2026

Sponsored By: Hubspot

This essay is brought to you by Hubspot. Revolutionize your workflow with 10 glorious Google Sheets templates, tailor-made for entrepreneurs and versatile marketers. From organizing your blog's editorial calendar to mastering paid media strategies and optimizing on-page SEO, these ready-to-use spreadsheets are here to make a difference. Be the change you wish to see in your spreadsheet.

I have a confession to make: I’m a biography bro. Folks like me read books galore on the famous and powerful, trying to divine the secret to these fabled individuals' success. On my shelf sit volumes on everyone from Mozart to Martin Luther King to Robert Moses. I have written book reviews in which titans of industry espouse their philosophies. After all, it is fun to learn how others came to make more money than me.

However, I worry that people have gotten a smidge ahead of themselves. In a recent conversation, a founder of a B2B SaaS company said to me in earnest that “reading about how Napoleon conquered Europe helped him run his company.” He’s not alone: there are podcasts and workshops, study groups and Substacks, all of them devoted to the discipline of the powerful. It is a harmless hobby, but it is a funny one.

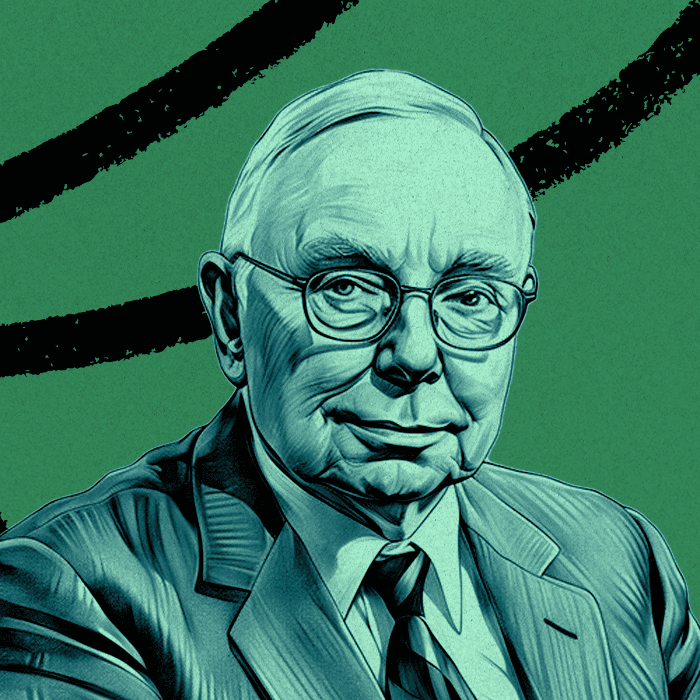

When Charlie Munger, the spiritual progenitor of the biography bro movement, died last week at 99, X was filled with hagiographies lionizing his legacy. The last week has bordered on—if not outright descended into—a period of spiritual mourning for Mungerites.

His philosophy is appealing, and his riches are undeniable. Munger, who had an estimated net worth of $2.3 billion, was the intellectual sparring partner of Warren Buffett, estimated net worth of $120 billion—and Munger, somehow, was noble enough not to murder Buffett over this difference in assets. Together they built Berkshire Hathaway, which has a market cap of roughly $775 billion. Not too shabby.

The key to his success? Mental models that are built by reading widely. To espouse his philosophy of success, 18 years ago he published Poor Charlie’s Almanac, a book of his teachings, that has been re-issued by Stripe Press. The whole thing is an ode to be being multi-disciplinary and widely read:

“You can’t really know anything if you just remember isolated facts and try and bang ’em back. If the facts don’t hang together on a latticework of theory, you don’t have them in a usable form. You’ve got to have models in your head. And you’ve got to array your experience—both vicarious and direct—on this latticework of models.”

Munger drew from the world’s well of knowledge to construct his models. In the reading list that accompanied the new edition, he included four biographies, and recent visitors to his home described shelves stuffed with profiles of the powerful. He, of course, read beyond this, with interests in psychology, mathematics, and biology.

Discover the power of efficiency with our Google Sheets templates, designed for the modern business landscape. Whether you're planning your next big marketing campaign or streamlining your content creation process, our templates have you covered. Experience the ease of an editorial calendar, delve into detailed paid media planning, and elevate your SEO efforts, all within a few clicks. These templates aren't just tools; they're catalysts for success.

And Munger’s own book is a repository of wisdom that argues for a distinct, pragmatic worldview. Many of my friends talk, at length, about how his writing has changed their lives.

I’ve read his book, done like Munger has done. The trademark wit and gumption he brought to his writing, with memorable lines like “being a one-legged man in an ass-kicking contest,” will be long lasting.

But I have a problem. I have absolutely no idea how to do what Munger says.

Thanks to our Sponsor: Hubspot

Thanks again to our sponsor Hubspot. Upgrade your potential with 10 exceptional templates, each crafted to enhance your business acumen. Say goodbye to the hassle of starting from scratch and hello to a world of streamlined processes and improved productivity. It's time to transform how you work, one spreadsheet at a time.

Create a free account, or log in.

Every members live and work at the edge of AI. Join now.

By continuing, you agree to the Terms of Sale, Terms of Service, and Privacy Policy.

Enjoy unlimited access to all of Every.

See subscription options