Evan Armstrong was a lead writer at Every who explored profit and power in technology in Napkin Math.

ITDA: The Gamification of Financial Statements

How governments and companies are engaged in mutual manipulation

May 28, 2021 · 11 min readUpdated Jul 28, 2026

TL;DR

- Welcome to my many new subscribers! Last week’s piece on Why You Shouldn’t Work at A Startup went semi-viral so a couple hundred fresh faces here today.

- Every other week, I publish a financial explainer where I go through the theory and application of financial concepts. We’ve been in the midst of a series on the income statement, with previous pieces covering Revenue, COGS, Gross Margin, and OPEX.

- Today we are covering four intimidating words ITDA (Interest, Taxes, Depreciation, and Amortization) that signal how well a company is playing the meta-level games of growth and capitalism.

- These Four Horsemen are all incentives created by governments in order to steer the behavior of businesses. Smart operators can utilize game theory and new software-powered services to save serious money.

The income statement starts with simple stuff, and gets increasingly shrouded in mystery as you work your way down.

At the top, we see Revenue (money customers give you), and then COGS (the direct cost to make the product you sell). After that you get into slightly murky territory with OPEX (the overhead costs to run the business), and beyond OPEX lies the true hidden chamber of the income statement—Interest, Taxes, Depreciation, and Amortization—which conceals a vast system of complex power games played by governments and corporations. In the context of an income statement, ITDA measures the skill with which a corporation plays the game.

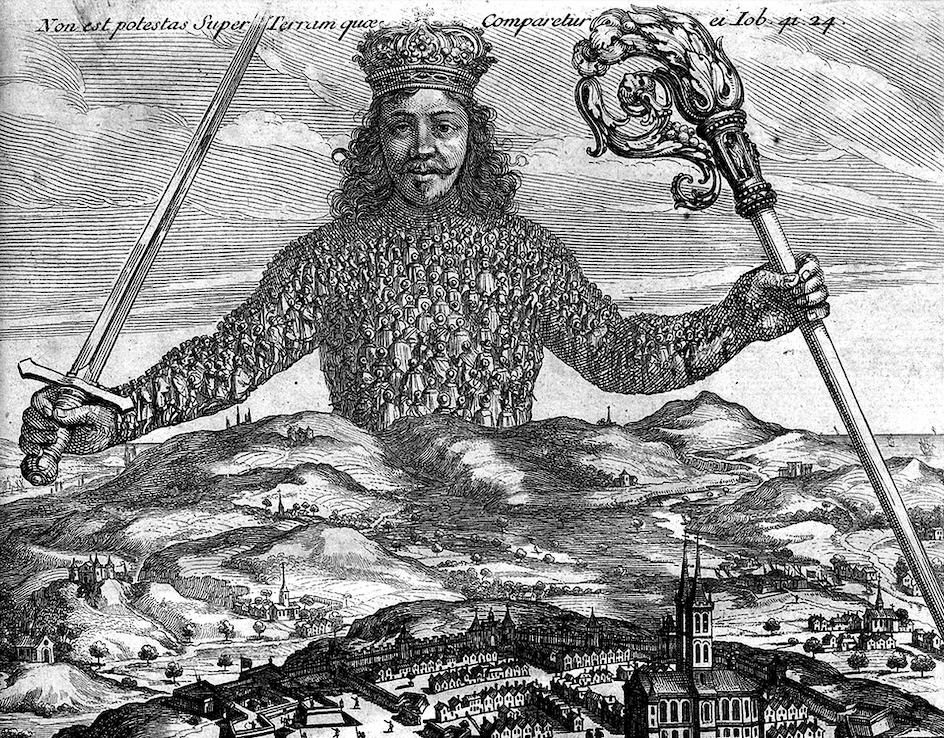

By participating in the American economic system, we passively opt-in to a series of social contracts that support society’s structure. Thomas Hobbes called these government-enforced contracts “the leviathan”—a monster of mythic power, armed with state-sponsored violence, that ensured the general populace were incentivized to do what they were supposed to. Note: I hear the political theorists whinging. Yes, this is an oversimplification/stretch, but I like this analogy so let me run with it. Go read some Kant you nerds.

Create a free account, or log in.

Every members live and work at the edge of AI. Join now.

By continuing, you agree to the Terms of Sale, Terms of Service, and Privacy Policy.

Enjoy unlimited access to all of Every.

See subscription options