Evan Armstrong was a lead writer at Every who explored profit and power in technology in Napkin Math.

The Zone of Deployment

How can you know when to invest?

Jan 25, 2024 · 4 min readUpdated Jul 10, 2026

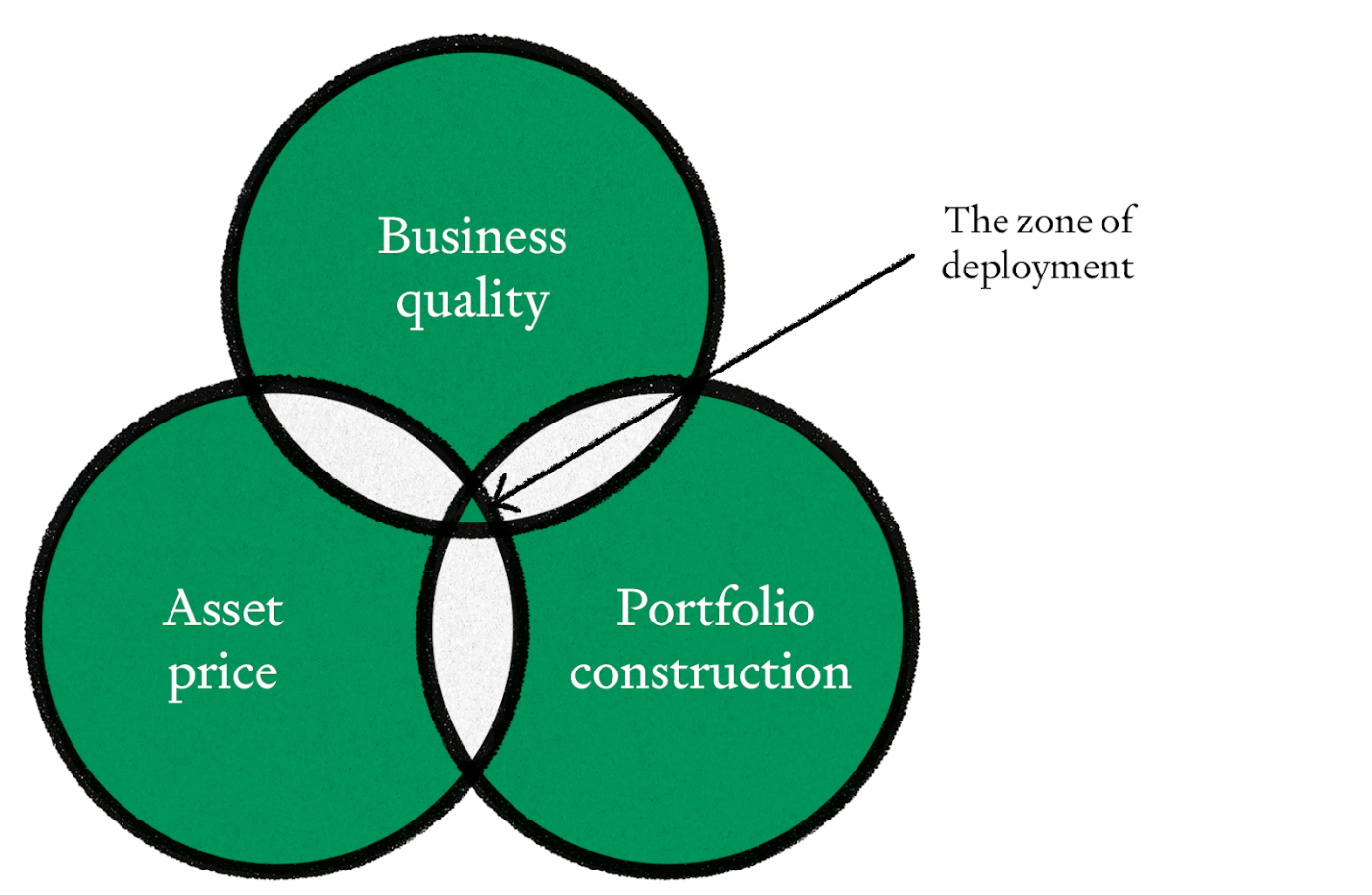

When you are looking to deploy capital, you have to keep three things in mind:

- Business quality: Is this a fundamentally strong business?

- Asset price: Does this price make sense?

- Portfolio construction: Does the opportunity cost outweigh the return?

It is only if all three of these things are fully understood that you can enter what I call the zone of deployment—the space where you should be willing to invest.

I don’t know if it is because David Fincher made such a banger with The Social Network or the VC content marketing machine is so relentless, but we’ve mostly focused on business quality over the last 10 years to the exclusion of the two other criteria. The stars of Facebook, Google, and Airbnb loomed so bright in our eyes that we began to believe that the only way to measure business quality was by a company’s ability to quickly scale to an enormous size. And we mostly funded startups we believed could achieve that.

The problem? Businesses that can “grow so fast nothing else matters” are more rare than you think.

Only 1 percent of startups return 10 times the invested capital. In public stocks, only 2 percent of public companies are responsible for 90 percent of the wealth creation in U.S. stock markets.

This means that if you want to get stupid rich via a venture-backed startup, you will need to select the 1 percent of the startups that raise seed capital every year—so one of the 80 of the 7,964 startups funded in 2023—and hold onto that equity for about 10 years. Then, even if you are lucky enough to have said company go public, you have to hope it becomes one of the roughly 10 companies that drive the majority of public stock returns. This math is a bit handwavy, but the Napkin Math™ for you to get wealthy off startups is about 2 percent public of 1 percent startup, for odds of .02 percent. Eek.

When I ran this math past my VC friends, they all said some variation of, “Those odds feel a little high.” Eek times two.

Create a free account, or log in.

Every members live and work at the edge of AI. Join now.

By continuing, you agree to the Terms of Sale, Terms of Service, and Privacy Policy.

Enjoy unlimited access to all of Every.

See subscription options