Evan Armstrong was a lead writer at Every who explored profit and power in technology in Napkin Math.

Tech stocks’ favorite lie to investors

How the LTV/CAC ratio is manipulated to take advantage of retail investors

Sep 9, 2021 · 11 min readUpdated Jul 16, 2026

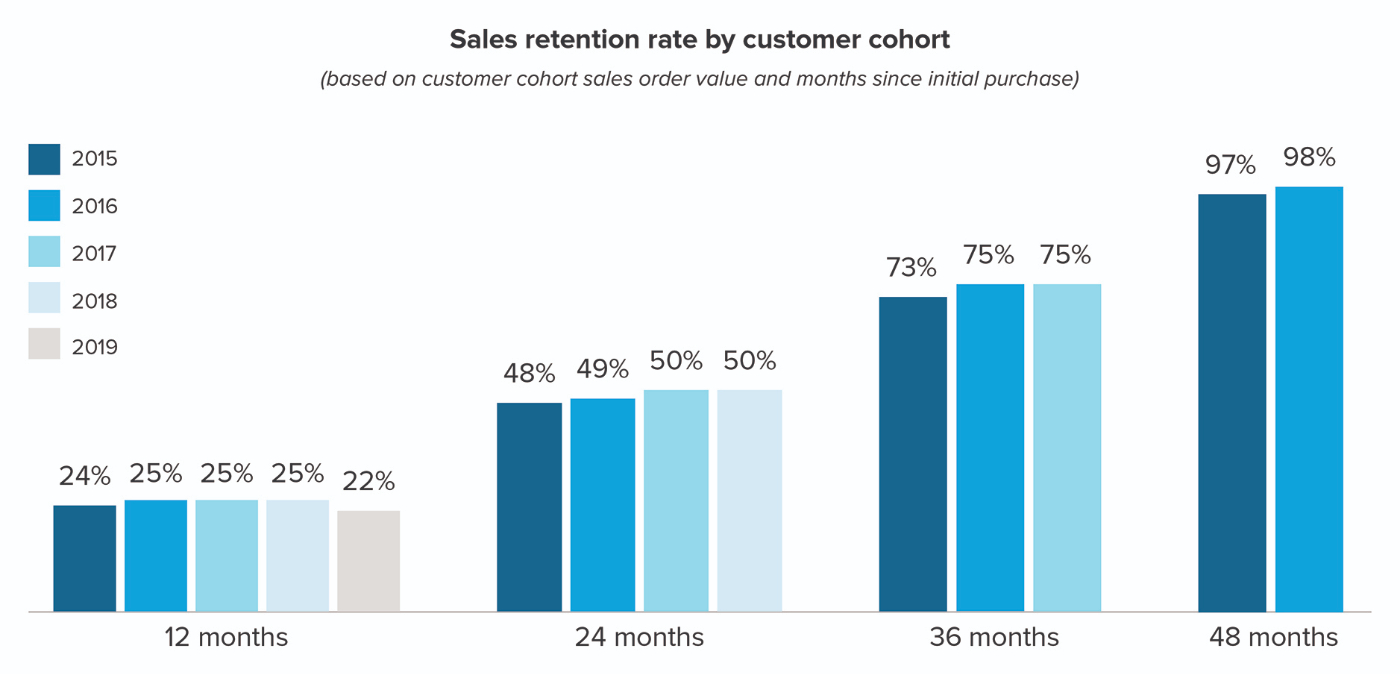

As a four-eyed nerd who spends my weekends analyzing businesses for fun, I was excited to see the Warby Parker S-1 drop. During my first read, I was having a great time. There were customer cohorts! Quips about how screens made our eyes rot and would increase their market size! Their average sales per square foot! (less cool but for the rule of threes I needed another thing to list). It was a veritable menagerie of business nerd dopamine hits.

One of the more impressive numbers was their customer acquisition cost (CAC). Pre-Covid they bragged a ~$27 CAC. Coupled with some best-in-class retention, this looked like a highly efficient growth machine, if you squint.

Any savvy investor will note this and build it into their assessment of the stock. But for retail investors who lack the skills/time, they will miss this and get taken advantage of.

Warby Parker is not the only sinner here. Recently, Figs (a clothing retailer) did the exact same thing in their S-1 back in May of this year. Their fib was identical by including repeat purchases and not just new customers into their CAC.

This behavior is mummery, an act, a falsification.

But the thing is, this isn’t unusual. In fact, companies lie in their SEC filings all the time. It’s an accepted part of the game.

And frankly, it pisses me off.

So today, we are once and for all showing exactly how the metrics used to define the Lifetime Value of Customer work, how to measure the acquisition costs to acquire a customer, and what good performance looks like.

Importantly, we’ll also show the common tricks that companies will pull to deceive people.

To do this, I teamed up with my good friend Spencer to tackle this issue. He is the perfect person to work with on this topic, having spent a few years at McKinsey advising major corporations on their growth, then owning the growth model for Stance Socks, a company doing $100M+ in top-line revenue, as their director of growth, and now advises startups on growth as an Associate at Upfront Ventures. Thanks to him for his time/effort/friendship.

We will start with the value a customer brings in, Lifetime Value (LTV), because knowing the money they bring is the first step so you have something to weigh the acquisition cost against.

If you would like to unlock the rest of the article, subscribe below. In addition to this article, you'll have access to Napkin Math's exclusive community and all of my archives. Your first month is only a dollar! Your subscription enables me to continue to write as an independent researcher.

Create a free account, or log in.

Every members live and work at the edge of AI. Join now.

By continuing, you agree to the Terms of Sale, Terms of Service, and Privacy Policy.

Enjoy unlimited access to all of Every.

See subscription options