Evan Armstrong was a lead writer at Every who explored profit and power in technology in Napkin Math.

Snapchat's Probably Screwed

Apple's ATT Fallout Continues

Jul 28, 2022 · 12 min readUpdated Jul 28, 2026

Sponsored By: Write of Passage

This article is brought to you by Write of Passage, an online course taught by David Perell designed to help you become a better writer and start building a reputation online.

Programming Note: Apologies this is coming out so late! Had a very sick puppy today, and as much as I love being on time when I post, I love my dog more. She is fine now—thanks for your patience!

Let’s look at some dire bullet points:

- Over the last 12 months, Snap stock is down ~87%.

- All headcount growth has been frozen

- The company refuses to give guidance for Q3

- It is currently trading for less than the price it IPO’d at five years ago (2017)

- It had a negative cash flow of $147M in Q2

- Simultaneously, it is doing $500M in stock buybacks (doing this while having negative cash flow is just a way to prevent dilution from stock-based compensation and prop up a stock price)

In times of crisis, founders are expected to rise to the occasion, to become wartime leaders, to lead their employees to glory and riches. Evan Spiegel’s response? Announcing a stock split that will allow him to sell shares without reducing his super-voting powers.

Ugh.

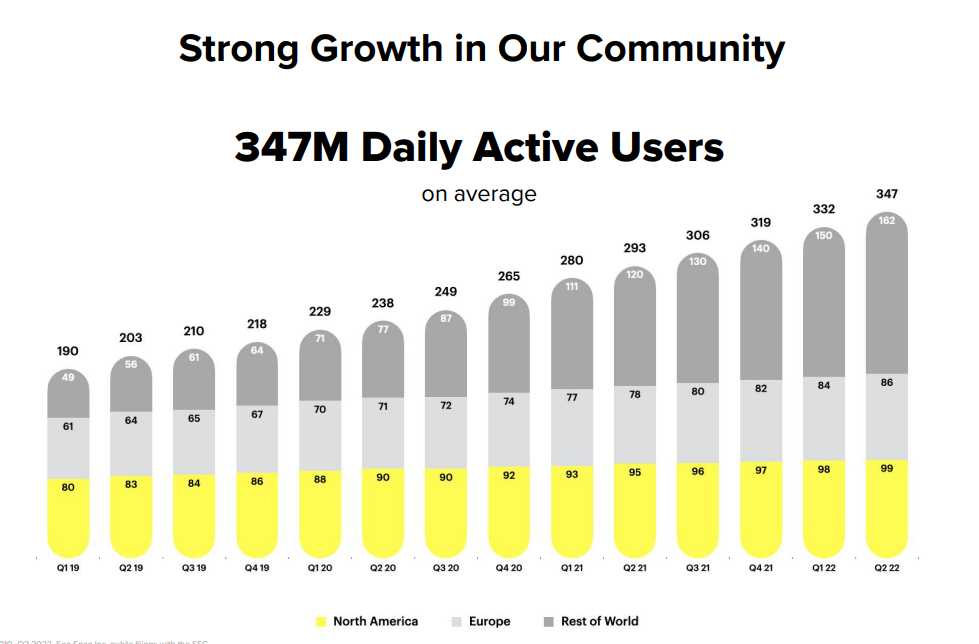

If you had predicted this outcome a few years ago, you would’ve been a laughingstock. Analyst reports on the company were full of hope, pushing the narrative of augmented reality (AR) and international growth. Investor presentations were filled with bold promises of a future where Snap was an advertising leader. They were so bullish that (only a year ago!) they promised to deliver 50%+ of yearly revenue growth. Instead, in Q2 they only delivered 13%. All of this points to a company that doesn’t understand what is happening to its own business.

Good writing is an unfair competitive advantage. Writers get more visibility online, and that visibility translates into their own personal monopolies. This newsletter itself is a testament to the power of writing online. I started from nowhere special and my writing has completely transformed my career.

If you are looking to improve your writing skills and start building your reputation online, then look no further than Write of Passage. It’s a course created by David Perell that will help you uncover your strengths, clearly communicate your value, and start gaining more visibility. Join thousands of other students like Packy McCormick and Ana Lorena Fabrega by accessing a free lesson from the course by clicking the link below.

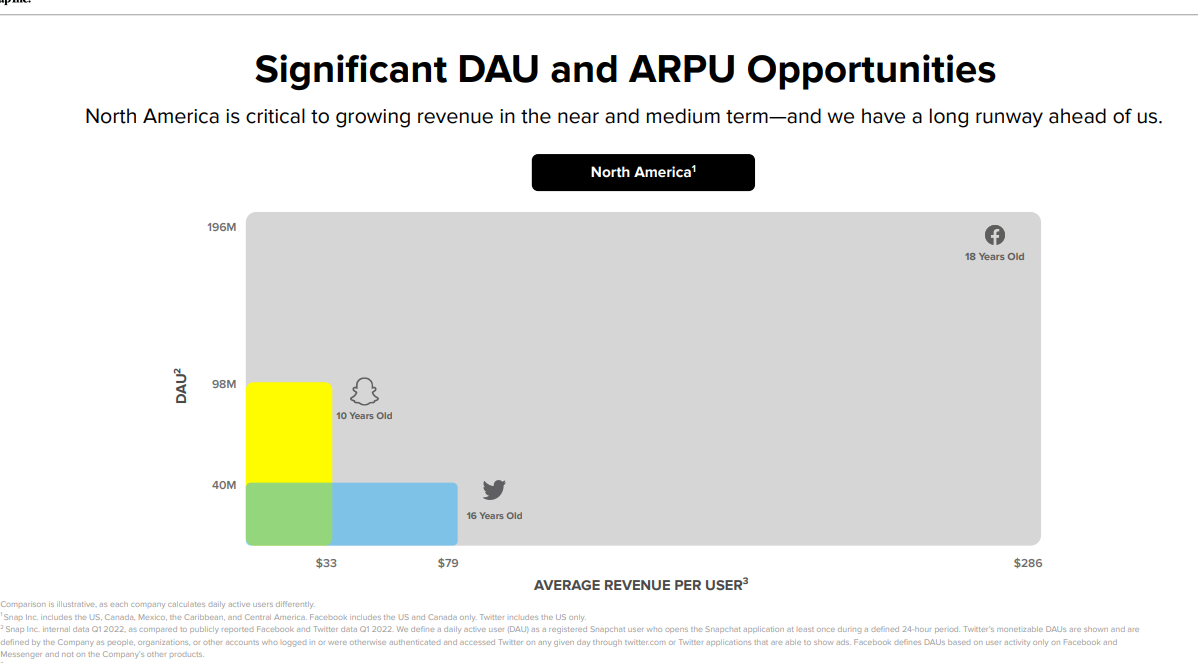

However, what has gone wrong isn’t a secret or some grand mystery. It is a combination of poor execution coupled with a fundamental misunderstanding of the digital ad market. Using the company’s most recent investor presentation as a visual aid, today’s piece will be in two parts. First an examination of their growth/product and second, an in-depth guide/analysis of their role in the digital ad market.

The problems start, unfortunately, at slide 1.

Positioning

Focusing the mission of the company on being a “camera company” has led the organization in a totally fruitless exercise of hardware development. Their first effort, the Spectacles, had an incredible marketing campaign in 2017. Popup machines dispensing the glasses were everywhere and the media was abuzz with how cool the launch was.

Even if you argued that a camera is the combination of hardware and software (and this is an argument I’m inclined to agree with) Snap is still missing 50% of the materials required.

All of this is a distraction, a narrative mirage to distract retail investors. This incorrect positioning is purposeful because it allows the company the room to burn cash on vanity projects and enjoy an innovation premium in their stock price. If you were to evaluate this as a media company that monetizes via ads, it is doing a laughable job. If you were to evaluate this as a camera company *I grimaced as I typed that phrase* then the whole social media thing is just a stepping stone to an AR future.

Ugh. Onto the next slide.

Really, the biggest competitive threat is TikTok, and while Snap has a similar video feed within its app, it doesn’t have the same power or capabilities as TikTok. The company's last exponential growth-inducing innovation was the stories format in October 2013. Everything since then has just been in the service of linear growth.

The problems don’t stop there. Monetization is busted too.

Ads, Ads, Ads

To understand why, you have to know how the digital advertising market works. I recognize that this goes fairly in-depth, perhaps a little more than is naturally comfortable, but the details really matter here. Snap has skirted by with surface-level analysis, but it is in the details of the ad market that the whole business falls apart. I’ll explain how it works and compare Snap’s capabilities to the gold standard of Meta.

Social media platforms’ ad efficacy is determined by 3 interrelated buckets of variables:

- Ad Performance: How well the average ad does on the platform and how measurable are those results

- Ad Inventory: How many slots and formats of ad space does the platform have to sell

- Ad Price: Whether ad inventory is determined via auction mechanics or contract sales

Ad Performance

Ad performance is determined by two variables: targeting and attribution. I wrote about this pretty extensively in a previous piece on Twitter, but a quick quote:

Create a free account, or log in.

Every members live and work at the edge of AI. Join now.

By continuing, you agree to the Terms of Sale, Terms of Service, and Privacy Policy.

Enjoy unlimited access to all of Every.

See subscription optionsThanks to our Sponsor: Write of Passage

If you are looking for ways to become a better writer and increase your visibility online, David Perell is here to help. To get started for free, he’s created a guide to help you discover your strengths, communicate your value, and build your reputation online. To get a free lesson from his Write of Passage course click the link below.