What You Need To Know About The Ant Financial IPO

The largest IPO in history is happening November 6th

Oct 30, 2020 · 7 min readUpdated Jul 25, 2026

Hey everyone! This week in Napkin Math we have a guest post from Yiren Lu and Grace Zhang about the upcoming Ant Financial IPO. Hope you enjoy it — let me know what you think in the form at the bottom of the post! — Adam

What: Ant is going public in a $35 billion IPO which would make it the biggest IPO in history. A spin-out of Chinese e-commerce giant Alibaba, they make software products that have democratized access to the financial system in China

When: November 6th

Where: Simultaneous listings on the Shanghai Stock Exchange and the Hong Kong stock exchange

Why is this interesting: The IPO is so massive—this reflects the fact that Ant touches nearly every aspect of Chinese financial life, especially for China’s 250 million unbanked citizens. It is also unique in the sense that Ant chose to list in China rather than in Hong Kong or the US.

✨ History of Ant:

💡Ant's Notable Products

Ant doesn’t just make one product—they make several. And their products don’t have easy to understand Western equivalents. Rather, each of their products can be seen as a sort of mash-up of the fintech products familiar in the U.S.

We’ve listed a few of the major products you should know about.

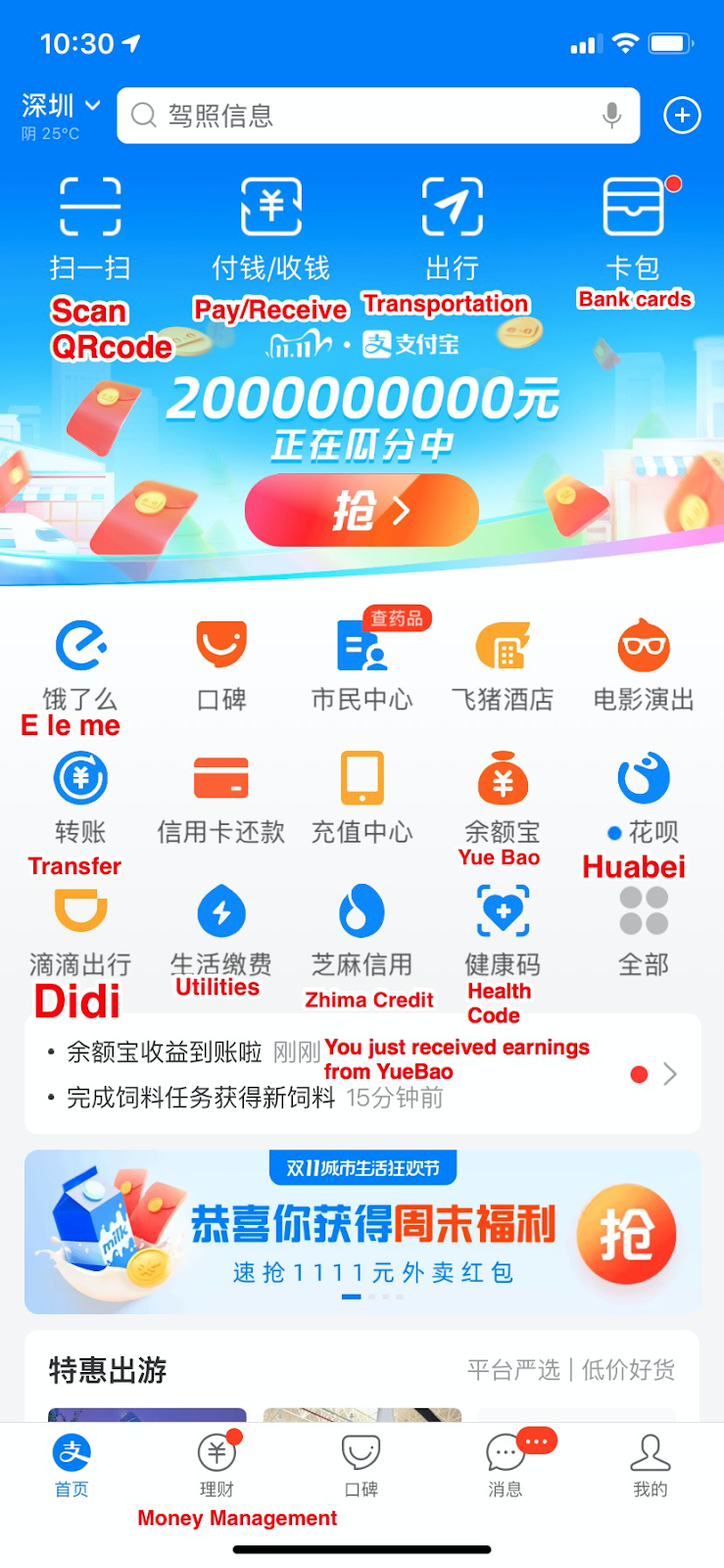

1 - Alipay Mobile Payments

Western Analog: Venmo + Apple Pay + Square.

People in China use Alipay for a variety of everyday transactions like:

Because of Alipay, Chinese consumers basically never have to swipe a credit card, pull out a physical wallet, or input payment information into a web form, the way that American consumers do. Every merchant, online and offline, takes Alipay and its main rival WeChat Pay.

Here’s what the main screen of Alipay looks like—it’s almost like its own operating system:

2 — Yu'eBao:

2 — Yu'eBao:

Another one of Ant’s notable products, Yu’eBao is a B2C money market fund launched in 2013.

Western Analog: A Venmo account that pays interest.

Why They Built It: More and more people were holding money in Alipay accounts—in the same way that many Americans have money in their Venmo account.

Ant found a way to allow Chinese consumers to earn interest on this money, rather than letting it sit around, by offering a money-market fund that they could buy into.

In order to do this they had to get around some tricky government regulations that prohibited payment companies from offering interest on their products.

Chinese consumers now effectively use Yu’eBao as a high-yield checking account: they can use it to pay for everyday expenses, and earn interest on their money at the same time.

Thought Bubble: When will their U.S. counterparts try to do the same?

3 — Ant Fortune

Create a free account, or log in.

Every members live and work at the edge of AI. Join now.

By continuing, you agree to the Terms of Sale, Terms of Service, and Privacy Policy.

Enjoy unlimited access to all of Every.

See subscription options