Evan Armstrong was a lead writer at Every who explored profit and power in technology in Napkin Math.

Selective Optimism

People who promise high returns forever are liars

Jun 16, 2022 · 8 min readUpdated Jan 31, 2026

This article is brought to you by Heyday, AI-powered research assistant that makes you smarter by automatically resurfacing content you forgot about.

Things are looking very, very bad out there.

For investors, it has been a rough year. Just in the last 60 days, we have seen tens of billions of investors' money destroyed by scams in Crypto like Luna. Tech company IPO prices over the last year are down ludicrous amounts, regardless if they were VC backed, SPACed, or PE backed.

Consumers are experiencing equal, if not greater, levels of pain. Last week, the national average mortgage rate hit 5.78%. It was at 5.23% just last week.

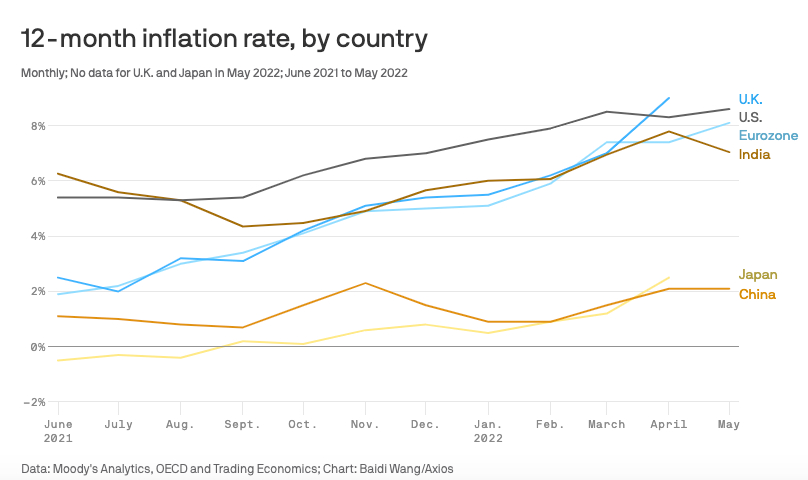

U.S. inflation is at its highest in 25 years with similar inflation rates being found globally:

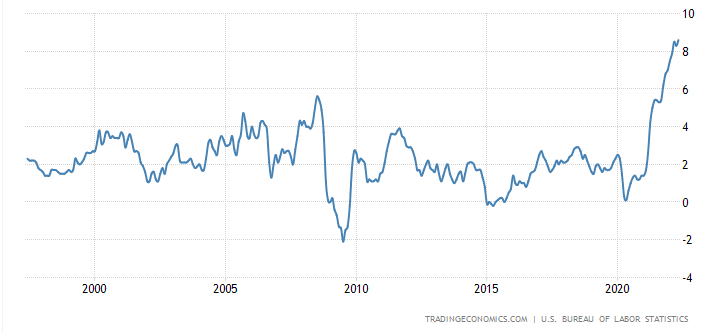

US Interest rates over the last 25 years

In response to this moment, friend of the publication Packy McCormick published a compelling post arguing for optimism. In many ways, I agree with him! You should be greedy when others are fearful! If you follow the trendlines and not the headlines, to quote Bill Clinton, this is actually a wonderful time to be alive. Opportunity is abundant! The world needs more optimism and I’m cheering on Packy for taking that challenge.

Sponsored by: Heyday

If you like to write and research online, you know how easy it is to lose track of relevant content you’ve encountered throughout your day. Heyday fixes that with a browser extension designed to help you learn faster and save time. It will:

- Surface content from past research alongside relevant Google search results

- Overlay articles you are reading with relevant tweets, articles, and documents

- Curate a knowledge base that fills itself with content related to topics you’ve spent the most time researching

Try Heyday for free, no credit card required.

However, if you are anything like me, whenever people tell you to be more optimistic, you bristle. There is something about this attitude that has big 1940s-grandpa-keep-your-chin-up-sport energy. It feels a smidge condescending. I recognize that part of this feeling is the narcissist in me that doesn’t like being told what to do, but there is also a component of the “choose optimism” narrative that is just plain wrong.

Entropy exists. Companies crater. Fundraises flop. It is very easy to be optimistic and poor (see NFT holders).

It may be the contrarian in me, but I think views espousing relentless optimism are simplistic and maybe even harmful. Being a default optimist or default skeptic is stupid. Determining when to be optimistic is smart.

Optimism is good, but sometimes it is a way for us to avoid hard truths. Too much optimism now and you might avoid a painful layoff today that leads to a company failure a few months from now. Or maybe too much optimism led you to take on too much risk in investing.

So today I would like to talk about two things. First, whether you should feel optimistic about this current market crash. It acts as a case study by which you can understand when optimism is bad. Second, I would like to walk through how optimism distorts the two most important variables in investment analysis: risk and return.

Why should you be optimistic right now?

If you are part of that 83% of consumer’s worrying about the economy, I have good news and good news. Good news numero uno is that you are right (congrats!) you should be worried about the economy. Good news two is that maybe, just maybe, you shouldn’t be worried about the economy personally.

To maybe make this more clear, an economy being in the pits is totally different than your personal finances being in the pits. An economy that is in a recession has decreased demand, lower asset prices, and mass layoffs. Unemployment shoots up and all the businesses propped up by cheap capital go the way of Aquaman after a late night (sleeping with the fishes). This is really, really scary for almost everyone.

However, it is a very happy time for some people for the exact same reasons. Unemployment is high (meaning cost of labor decreases), businesses die (decreasing the amount of competition), and asset prices are down (meaning that it is cheaper to acquire assets). I know so many people that became millionaires during the Great Recession. Right as the market bottomed out they went hard with their capital reserves and bought and bought and bought. A real estate fund that I’m familiar with spent hundreds of millions in 2010 on rental housing purchases in Phoenix and Las Vegas, two of the areas hardest hit by the Recession, and have made an absolute fortune.

Whether you should be optimistic during a recession actually has little to do with the overall state of the economy and more to do with the state of your personal economy. If you can ride out a few years of decreased wages and more expensive bills, then you are ready to rock and roll. If you have capital to deploy it is great!

Another important point that I feel compelled to make as we discuss this market downturn: Public stocks are not for sale!! I keep seeing people saying this on Twitter and it is bugging me. Yes, stocks cost less than they used to but that is not equivalent to them being for sale. Them being for sale would require that they are being sold at a price cheaper then what they will be in the future. Picking individual stocks as an investment strategy still sucks, even in a bear market. If you have excess cash that you will not need to touch for 5+ years I would be buying into index funds. A recession does not suddenly make you the next Warren Buffett—you are not capable of being a successful trader. Stop it. Go buy index funds at a consistent pace every month and quit trying this stupid strategy. The thing that matters is time and compounding. Price is relatively unimportant in comparison with patience.

This is another case of where optimism can go awry. The idea that things are cheaper is true—in aggregate. In isolation—how on earth can you tell? Why does a decrease in GDP suddenly make you a good asset evaluator?

Thanks to our Sponsor: Heyday

You need to reference an article you read before but can't find it, what do you do? Check out Heyday, the browser extension that remembers for you. It automatically saves the pages you visit and resurfaces them when you need them most.

Create a free account, or log in.

Every members live and work at the edge of AI. Join now.

By continuing, you agree to the Terms of Sale, Terms of Service, and Privacy Policy.

Enjoy unlimited access to all of Every.

See subscription options