Today’s post is a collaboration between Napkin Math and Byrne Hobart’s The Diff.

Where Netflix Is

The Netflix Model Today

There is perhaps no more colossal waste of human potential than Netflix. An algorithmic content feeding tube, designed by Silicon Valley engineers to deposit dopamine into our lizard brains at the exact point that we would churn, Netflix’s final form will be a pair of wires shoved directly into our eyeballs giving us personally crafted reality television. I love it. Its service is paid for by over 222M viewers (with millions more gleefully pirating the content like they are Limewire in 2005). The stock price has been one of the highest performing of the last 20 years. It has single-handedly sparked a television and film creative renaissance.

Whenever a new technology enables a fresh media paradigm, companies initially compete on an axis of distribution. The first televisions were distributed to American consumers with few channels. Media companies produced relatively bland and benign materials. News programs largely consisted of someone reading the headlines while smoking a cigarette. Howdy Doody held dominance in American children's consciousness for over 10 years just by being in color. Over time, as companies grow more comfortable with a new technology/medium, the bar for content quality is raised. Competition shifts from being able to use a technology to being able to use it effectively. Howdy Doody, despite being the first program to embrace color TV, was slayed by The Mickey Mouse Club.

Whether you view Netflix as a humanities catastrophe or entertainment’s pinnacle, there is no denying that it is an incredibly impressive business. By making streaming the dominant form of premium video consumption, Netflix embraced a new technology that catapulted them to the top of the world. Now the axis of competition has shifted to the second phase. Numerous companies have (mostly) figured out how to stream successfully. Their competitors are 10 times their size, have hundreds of billions of dry powder ready to deploy, and are willing to pay to win. This question is especially potent now—Netflix has missed on forecasted subscriber growth and has seen its stock price drop by 40%+ since November. Meanwhile, their rodentesque competitor Disney+ added 12M subscribers just last quarter. Whether Netflix is the winner of the future or is killed by Disney just as Howdy Doody was, is the subject of this essay.

CAC and LTV: How Auteurs Collaborate With Quants

Like any subscription company, Netflix lives and dies by one core calculation: the cost of customer acquisition relative to the lifetime value of a customer. Unfortunately for analysts, this number is incredibly hard to calculate even internally—and Netflix doesn’t release some of the data you’d want in order to measure it, even at a high level.

A shorthand approach to the LTV/CAC equation is to treat a company’s product and overhead costs as fairly fixed, and to look at the marketing costs to acquire an incremental customer, and then calculate a) the annual gross profit from that customer, and b) how likely the customer is to quit the service.

That’s always a fuzzy approach, because the cost of product development isn’t constant; companies do get operating leverage, but tend to increase their R&D expenses right along with sales. (In fact, for other subscription-based companies like Salesforce and Spotify, annual growth in R&D spending is higher than revenue growth; as the product matures, it takes more and more effort to build new features that will capture incremental customers.)

For Netflix, this equation is particularly complicated because their biggest cost, acquiring content, is also the lever that moves both user acquisition and retention. The company has had counterintuitive user acquisition and retention drivers for a long, long time; this dynamic actually predates their streaming business.

Back in 1999, when Netflix was still a DVD-by-mail company, one of their theories was that faster delivery would pay off because it would improve customer retention. When they started, customers in San Jose got their DVDs right away, while customers in, say, Florida had a longer wait. So the company did an experiment, and started dropping off DVDs at the Sacramento post office, too, to see if that would increase retention.

It didn’t.

Instead, it increased growth: new Netflix subscribers were more likely to brag about the service if they got instant gratification, but by the time they were regular subscribers they’d settled into a rhythm of stocking up on DVDs they knew they’d want to watch someday, not the ones they needed to see right away.

Today, churn and user acquisition are still determined by a complex mix of factors, with content playing an important role. Here’s how one Tegus call describes it:

[S]omebody that has 25 or 30 hours on a streaming service is very likely to remain engaged. Somebody that has fewer than 10 hours on a service is very likely to churn. And so then somebody who has 50 hours of engagement might not be that much more likely to retain than somebody who has 30 hours. So [the question on content’s value is] what's enough content for each user.

And this changes over time, both by market and by user. From the same call:

>[L]et's say, you are in an emerging market, so you're not fully penetrated, then you'd say, well, the first tranche of subscribers to Netflix will be younger, they might be more city dwelling versus country dwelling. You sort of say, well maybe there's this profile. And if we can nail that profile, we can expand outwards because people will be talking about the shows.And so that may push you towards edgier, younger adult content or darker content or content with bigger premises. As you grow in markets, you sort of may say, well, we're whatever, 30%, 40%, 50% penetrated, we're going to start looking more like TV in general.

And later:

>[A] high-quality returning series that people love will sort of tend to shift from an acquisition vehicle to a retention vehicle as the series matures.

Over time, especially for a company that’s getting close to full penetration of its biggest markets, churn matters more than customer acquisition. Which means that in a market like the US, the shows that are least talked-about relative to when they started are proportionately most important to keeping customers around. The maximum return on Squid Game or The Tiger King doesn’t necessarily happen when it’s trending on Twitter, getting talked about at parties, or creating opportunities to pump and dump small cap stocks. It’s when the show is tired and boring to tastemakers, but still has a loyal following that will keep their Netflix subscription in anticipation of the next season.

The variable returns from different kinds of content create some fun nonlinearities in Netflix’s returns. Suppose that one year there’s a popular Spanish-language show about Instagram influencers married to a famous soccer player.If that adds a new cohort of users, but those users aren’t engaging much with other content, then suddenly the relative returns of more Spanish-language social-media-influencer-married-to-athlete content soars. If there’s enough of it to push people to the 20- or 30-hours-a-month threshold, it pays, and if there isn’t, those subscribers leave.

Over time, cohorts will get more generic in some ways and more hyper-specific in others:

- Even if someone joins to watch one kind of show, such that showing them another one in that micro-genre is a measurably good deal, they’ll probably branch out over time. Netflix relentlessly collects data on what people like to watch, and will find the other overlaps; maybe some of those viewers like reality TV, others are willing to consume fact or fiction about the perils of fame, and others are just really into soccer.

- At the same time, once they’re addicted to a particular show, the returns from one more season of that show are more predictable.

Today’s post is a collaboration between Napkin Math and Byrne Hobart’s The Diff.

Where Netflix Is

The Netflix Model Today

There is perhaps no more colossal waste of human potential than Netflix. An algorithmic content feeding tube, designed by Silicon Valley engineers to deposit dopamine into our lizard brains at the exact point that we would churn, Netflix’s final form will be a pair of wires shoved directly into our eyeballs giving us personally crafted reality television. I love it. Its service is paid for by over 222M viewers (with millions more gleefully pirating the content like they are Limewire in 2005). The stock price has been one of the highest performing of the last 20 years. It has single-handedly sparked a television and film creative renaissance.

Whenever a new technology enables a fresh media paradigm, companies initially compete on an axis of distribution. The first televisions were distributed to American consumers with few channels. Media companies produced relatively bland and benign materials. News programs largely consisted of someone reading the headlines while smoking a cigarette. Howdy Doody held dominance in American children's consciousness for over 10 years just by being in color. Over time, as companies grow more comfortable with a new technology/medium, the bar for content quality is raised. Competition shifts from being able to use a technology to being able to use it effectively. Howdy Doody, despite being the first program to embrace color TV, was slayed by The Mickey Mouse Club.

Whether you view Netflix as a humanities catastrophe or entertainment’s pinnacle, there is no denying that it is an incredibly impressive business. By making streaming the dominant form of premium video consumption, Netflix embraced a new technology that catapulted them to the top of the world. Now the axis of competition has shifted to the second phase. Numerous companies have (mostly) figured out how to stream successfully. Their competitors are 10 times their size, have hundreds of billions of dry powder ready to deploy, and are willing to pay to win. This question is especially potent now—Netflix has missed on forecasted subscriber growth and has seen its stock price drop by 40%+ since November. Meanwhile, their rodentesque competitor Disney+ added 12M subscribers just last quarter. Whether Netflix is the winner of the future or is killed by Disney just as Howdy Doody was, is the subject of this essay.

CAC and LTV: How Auteurs Collaborate With Quants

Like any subscription company, Netflix lives and dies by one core calculation: the cost of customer acquisition relative to the lifetime value of a customer. Unfortunately for analysts, this number is incredibly hard to calculate even internally—and Netflix doesn’t release some of the data you’d want in order to measure it, even at a high level.

A shorthand approach to the LTV/CAC equation is to treat a company’s product and overhead costs as fairly fixed, and to look at the marketing costs to acquire an incremental customer, and then calculate a) the annual gross profit from that customer, and b) how likely the customer is to quit the service.

That’s always a fuzzy approach, because the cost of product development isn’t constant; companies do get operating leverage, but tend to increase their R&D expenses right along with sales. (In fact, for other subscription-based companies like Salesforce and Spotify, annual growth in R&D spending is higher than revenue growth; as the product matures, it takes more and more effort to build new features that will capture incremental customers.)

For Netflix, this equation is particularly complicated because their biggest cost, acquiring content, is also the lever that moves both user acquisition and retention. The company has had counterintuitive user acquisition and retention drivers for a long, long time; this dynamic actually predates their streaming business.

Back in 1999, when Netflix was still a DVD-by-mail company, one of their theories was that faster delivery would pay off because it would improve customer retention. When they started, customers in San Jose got their DVDs right away, while customers in, say, Florida had a longer wait. So the company did an experiment, and started dropping off DVDs at the Sacramento post office, too, to see if that would increase retention.

It didn’t.

Instead, it increased growth: new Netflix subscribers were more likely to brag about the service if they got instant gratification, but by the time they were regular subscribers they’d settled into a rhythm of stocking up on DVDs they knew they’d want to watch someday, not the ones they needed to see right away.

Today, churn and user acquisition are still determined by a complex mix of factors, with content playing an important role. Here’s how one Tegus call describes it:

[S]omebody that has 25 or 30 hours on a streaming service is very likely to remain engaged. Somebody that has fewer than 10 hours on a service is very likely to churn. And so then somebody who has 50 hours of engagement might not be that much more likely to retain than somebody who has 30 hours. So [the question on content’s value is] what's enough content for each user.

And this changes over time, both by market and by user. From the same call:

>[L]et's say, you are in an emerging market, so you're not fully penetrated, then you'd say, well, the first tranche of subscribers to Netflix will be younger, they might be more city dwelling versus country dwelling. You sort of say, well maybe there's this profile. And if we can nail that profile, we can expand outwards because people will be talking about the shows.And so that may push you towards edgier, younger adult content or darker content or content with bigger premises. As you grow in markets, you sort of may say, well, we're whatever, 30%, 40%, 50% penetrated, we're going to start looking more like TV in general.

And later:

>[A] high-quality returning series that people love will sort of tend to shift from an acquisition vehicle to a retention vehicle as the series matures.

Over time, especially for a company that’s getting close to full penetration of its biggest markets, churn matters more than customer acquisition. Which means that in a market like the US, the shows that are least talked-about relative to when they started are proportionately most important to keeping customers around. The maximum return on Squid Game or The Tiger King doesn’t necessarily happen when it’s trending on Twitter, getting talked about at parties, or creating opportunities to pump and dump small cap stocks. It’s when the show is tired and boring to tastemakers, but still has a loyal following that will keep their Netflix subscription in anticipation of the next season.

The variable returns from different kinds of content create some fun nonlinearities in Netflix’s returns. Suppose that one year there’s a popular Spanish-language show about Instagram influencers married to a famous soccer player.If that adds a new cohort of users, but those users aren’t engaging much with other content, then suddenly the relative returns of more Spanish-language social-media-influencer-married-to-athlete content soars. If there’s enough of it to push people to the 20- or 30-hours-a-month threshold, it pays, and if there isn’t, those subscribers leave.

Over time, cohorts will get more generic in some ways and more hyper-specific in others:

- Even if someone joins to watch one kind of show, such that showing them another one in that micro-genre is a measurably good deal, they’ll probably branch out over time. Netflix relentlessly collects data on what people like to watch, and will find the other overlaps; maybe some of those viewers like reality TV, others are willing to consume fact or fiction about the perils of fame, and others are just really into soccer.

- At the same time, once they’re addicted to a particular show, the returns from one more season of that show are more predictable.

Churn is not just driven by show count, which is under Netflix’s control; it’s also driven by trends in screen count, which are outside of the company’s control but have been moving in a favorable direction for a long time. Netflix has been talking for over a decade about the benefit of multiple screens. From a 2010 earnings call: “Lots of people come back to finish movies and TV shows. They will be watching on the television and then they're in the car, and they finish on the iPod and Touch, or the iPhone and there are all those different -- they move to a different room and they get to restart and of course our software is smart enough to restart them in the right place…for us they are all just screens. There are four-inch screens that are on mobile phones, there's nine-inch screens on iPad, 12-inch screens on laptops, and then a wide variety of television-size screens from 20 to 100 inches. And, that is not a key determinant it for us and not something that I can give any more color on.”[x]

Part of the beauty of the Netflix model is that it can afford more artistic experimentation upfront because it’s engaged in a constant effort to train a recommendation engine. A library of thousands of movies and shows means that there’s a superabundance of choices, which can lead to zombie-like endless scrolling. Even narrowing Netflix’s US library down to the best 1% of options means that choosing what to watch requires fifty choices about what not to watch. Netflix has gotten famously good at recommending content, not only matching people to what they’re likely to enjoy but to what pitch they’re going to enjoy (this post summarizes some examples of cover art that won the A/B tests, while this one goes into a surprising amount of detail on exactly how to run such an A/B test—are you maximizing clicks, or watch time? And what exactly constitutes a “different” piece of cover art?)

What’s counterintuitive about this is that a relentless testing-driven approach is actually a great complement to artistic free expression, at least for season 1 of a show and for the first movie in a franchise: a compelling new feature in artistic terms will have informative features in machine learning terms, so it doesn’t just produce additional watch time, but additional data that can convert into more watch time for other recommendations.

So estimates of Netflix’s unit economics are tricky on the inside and very subjective from the outside. Annoyingly, the company used to break out more useful data–until 2012, they disclosed monthly churn, which tended to be in the 3.5%-4.5% range.[x] We can use the seasonality from when Netflix disclosed their churn, and the more recent approximations from Antenna, to roughly estimate Netflix’s churn and seasonality, and then we can assume a gradual decline in churn as Netflix gets a bigger content library and better data. All this gets us to a gross subscriber increase number. And that lets us look at some approximate CAC trends.

Historical data via Daloopa, churn from author estimates using historical seasonality and recent data from Antenna.

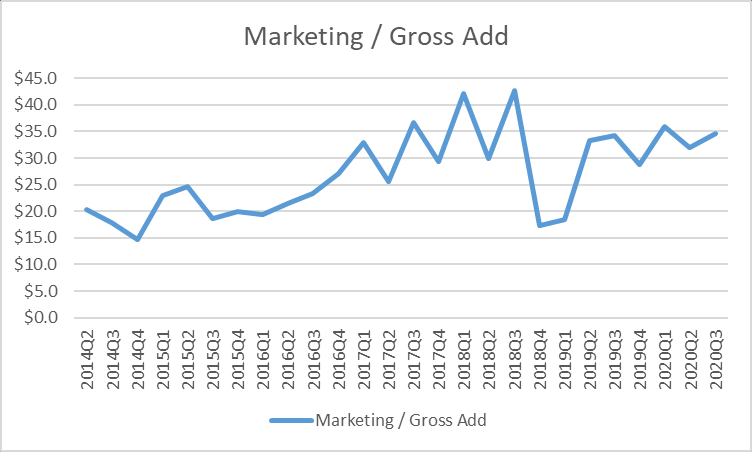

It’s trickier to benchmark their content spending to gross adds. Over time, using the same metrics, the content dollars required to drive an incremental customer went from $95.30 in Q2 ‘14 to $162.96 in Q4 of 2021. Of course, that content also affects user retention, but since we don’t have either a) precise churn numbers, or b) a good breakdown of how content’s benefits are apportioned between new viewers and existing ones, we can’t realistically estimate this.

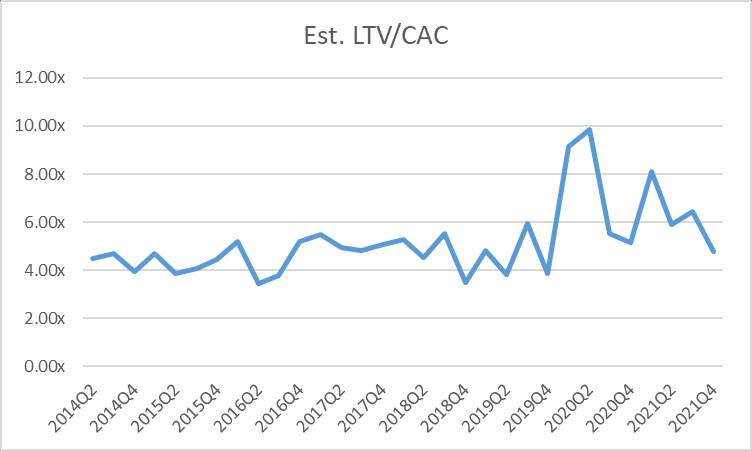

We can look at estimated churn rates and the company’s gross profit per subscriber to get another look at unit economics, and this actually shows a promising trend (again, it’s using an estimated churn rate, not a real number, but the relative stability of the LTV pre-Covid is a good sign that those churn estimates are approximately right):

In this model, we’re looking at (actual) gross profit for a customer’s (estimated, undiscounted) lifetime value, compared to their (actual) marketing cost per (estimated) gross subscriber addition. Netflix’s gross profit calculation accounts for the amortization of their content assets, and that amortization number is driven by estimates of the useful life of their content assets. So it’s an approximation that relies on trusting both the company’s estimates and mine, but looks roughly intuitively right: the company was consistently spending marketing dollars when they could get incremental profits equal to about 4x-6x that spending, though during Covid the organic improvement in signups outran their ability to spend marketing money fast enough.

In light of that, Netflix’s recent decline in valuation looks a lot like other post-Covid returns to normality, where investors have concluded that some of the growth was pulled forward, while some of it was real; in cases where that pulled-forward growth did not require heroic increases in fixed costs or inventory (e.g. for Zoom), that meant the company was returning to a higher steady-state. In cases where the Covid spending boom forced the company to take some inventory risk and increase fixed costs substantially (as with Peloton), the company’s value could be reset to a lower level than during Covid. Netflix was a net beneficiary of the pandemic, just less than it looked like at first.

Competition

Let’s say you gave a billion dollars to each content team at Apple, Disney, Paramount, Peacock, HBO, Amazon, and Netflix. They get to keep all of their organizational structure, subscribers, and previous IP. Who wins? You could probably argue HBO with their legacy of shipping unique content. Another reasonable take is that Disney could simply lean on its legacy IP. (Peacock is never the right answer).

This is actually a bit of a trick question—we never defined what winning meant. If such competition were actually to occur, Amazon’s team would inform their executives of their objective to which their likely response would be, “How will your Lord of The Rings show help us sell more toilet paper?” Meanwhile, Disney executives would probably take half the team's budget and promptly give it to the Marvel division to go make another Iron Man movie. They would then use the other half to pump Disneyland tickets to foolish parents.

It is tempting when considering the competitive landscape to reduce the comparison to be the efficiency of the creative output. Most of the takes (prominently Ben Thompson over at Stratechery) argue that Netflix will be the winner of the content wars by virtue of lowest cost per subscriber. Netflix may not have the unique IP of Disney or the cash of Apple, but they have the largest subscriber base by which they can spread out their content costs. A $100M dollar show for HBO Max (73.8M subscribers) costs $1.35 per subscriber. Netflix (222M) producing the same video, at the same cost, gives you a cost per subscriber of $.45.

However, almost every streaming service besides Netflix comes at the problem not from a dollar efficiency perspective but more from a bundled products viewpoint. E.g. Disney wants you to watch the new Loki show on Disney+, order merch through their e-commerce store, wear that merch to the new Avengers portion of Disneyland, and then post about it all on social media. As we discussed earlier, Netflix calculating its LTV/CAC ratio is a near-impossible task just by charging a flat fee. Can you imagine the complication that occurs when trying to guess the LTV/CAC for Amazon? While efficiency matters, so do the efficacy of the dollars produced.

When considering the question of competition, it must be approached from a perspective of IP monetization methods. These break down into three groups of direct competitors:

Subscription focused: These are the companies that are in for a world of hurt. They are selling a product identical to Netflix with half of the subscriber base and a smaller content backlog. Going head to head with nothing differential besides saying “We have the Office!” is a challenging strategy. This is Peacock and Paramount+. There is always riches in Niches, such as anime subscription service Crunchyroll (5M paying subs), but for the platforms that are attempting to be generalists going after Netflix’s turf we wish you good luck and godspeed.

The one exception to the struggles of the other platforms is HBO Max (73.8M subs). They have been able to carve out a significant portion of the market for themselves. However, it took them having a distribution partnership with their parent company AT&T, putting every major blockbuster from the studio on the platform, and knocking it out of the park from a creative perspective. Note: Mare of Easttown was particularly good last year.

Native Attribution: This the Disney+ category. The House of the Mouse views Disney+ as one part product line, one part marketing department. Among all of the other competitors they have the most ways to leverage their IP into additional revenue streams. If you’ve been to any of the Disney parks recently, you’ll know exactly what we are talking about. Attendees walk around festooned with merch proclaiming royalty to one franchise or another. Their latest offering is a Star Wars immersion hotel. It will connect to the latest shows happening on Disney+ and the larger star wars universe. The price tag is 4800 dollars for the 45 hour experience. If that simply isn’t enough Disney for you, the company announced on Feb 16th its plans to make residential communities. The first community will be built in the Coachella Valley with up to 1900 homes. Disney+ is a direct product competitor but the role that it acts as only one part of the larger disney experience.

Indirect Benefits: This is the major tech platforms realm. Drawing the link between how many iPhones or Apple TV’s are sold because someone is an Apple TV+ subscriber is near impossible. Similarly it is difficult to point to what % of Amazon Prime subscribers don’t churn because they have access to Prime Video. However, these companies are sitting on so much cash, and they understand on a gut level the power of attention, they are willing to compete even if the math isn’t completely clear. They are also willing to spend big—Amazon has reportedly earmarked over a billion dollars just for the upcoming Lord of the Rings series.

The final competitive consideration for Netflix is the role of entertainment. Famously, Reed Hastings, Netflix’s CEO, stated that “We compete with (and lose to) Fortnite more than HBO.” To be fair, he said this in 2019, but the point still stands. Anytime you are on a device doing something besides binging Stranger Things, you are giving your attention to a competitor of Netflix. Videogames, Youtube, TikTok, all of these services take eyeball hours away from the company. Netflix has plans to address some of these deficiencies (more on that in a minute) but the point remains. Netflix has to compete with the best alternative for entertainment, spread across all the different ways that humans are entertained.

In summary, we are of the opinion that Netflix is the winner among the streaming-focused platforms. However, what winning looks like when you are competing with firms who use streaming to push other product lines is unclear. The end result will be fine for Netflix. The average American spends $47 a month on streaming services, Netflix will almost certainly always be a part of that bundle.

Where Netflix is Going

What Else Can Netflix Sell?

Netflix is not unaware of these competitive dynamics. It is cognizant of the threat that comes from all these different modalities stealing eyeball time. In response, they have started to dip their toes deeper and deeper into other media formats. There are a variety of attempts—from a magazine publication called Queue that is devoted exclusively to the fandom of Netflix programming. They also have a Netflix Merch store (with the backend run off of Shopify) launched in June of 2021. Both of these feel like fun little experiments right now versus the major investment required to make any material difference for their financial performance.

What is most interesting is Netflix’s push into video games. Netflix has some video content based on video game-centric properties (stuff like the Witcher and a new Bioshock movie). To be clear, we are specifically talking about their new video game division. Headed by a former EA executive, the strategy is still fairly nebulous, but reports have said that the company’s thoughts are focused on hosting the games in-app. They will be included in the price of a Netflix subscription.

If you return to the “Indirect Benefits” category of competition, each of the big tech companies has its own version of game streaming platforms. Most prominently, Microsoft has Gamepass as the tent pole of their video game strategy. It allows gamers to play AAA games on both consoles and PCs. Amazon has an identical (but far less popular) service called Luna that allows players to game where they deem best.

The best comparison is probably Apple’s Arcade offering. This is a subscription that allows exclusive, ad-free access to 100+ games, exclusively on iPhone for $4.99 a month. If you squint and swap out a few nouns, this is an identical pitch for Netflix. Regardless, the service, despite being debuted with a bang in 2019, has largely shuffled along with no real breakout hits. Apple has never disclosed the size of the subscription base. Seeing how subscriptions are the big story on Apple’s earnings calls, if the program had a modicum of success they likely would have discussed it by now. This lack of public discussion, coupled with a content strategy pivot the service underwent last year away from originals, suggests to us that this service has largely been a miss.

The lesson is that gaming is still incredibly, horribly difficult to compete in. Breakout hits are so incredibly rare that we find it difficult to assume that this new modality will be able to beat back the giants of Microsoft/Activision and Sony. Netflix will be able to produce games that enrich their IP, but will they be able to meaningfully reduce the amount of time teenagers spend on Fortnite? It’s unlikely.

If the mobile gaming component is unsuccessful, what remaining options does Netflix have with gaming? Rather than leaning into a pithy mobile experience, we would suggest the firm should lean hard into other gaming modalities. The easier option would be the Disney route. Disney has had similar troubles with turning its IP into successful franchises. After many failed attempts, Disney has settled into licensing their IP to outside game studios and taking a cut of the revenue. Netflix could do the same. We would play a Squid Game RPG or some other video game they license.

The second option is the more risky option. Instead of licensing, they could buy game studios. Netflix has shown that they are willing to swing big, often throwing down tens of millions on unproven entertainment talent. Why not place similar bets in the video game system? Building cross-platform games that leveraged Netflix IP while simultaneously profiting from the upside seems like an obvious option.

Either option eventually comes down to the core LTV/CAC calculation. Would it be better to spend 500M on gaming or on trying to find the next Tiger King?

Going Global

Any business with high fixed costs and low marginal costs wants to expand to the largest possible market. So going global is inevitable. For Netflix, this took a surprisingly long time. In his memoir, That Will Never Work, Netflix cofounder Marc Randolph refers to “The Canada Principle” to describe low-priority tasks: yes, expanding to Canada would add a mostly English-speaking market that was 10% larger than Netflix’s then-US-only market, but it wasn’t the kind of move that would produce the highest possible returns. Netflix did reach the Canadian market in September of 2010, and expanded to Latin America in late 2011, then added a European beachhead with the UK and Ireland in 2012. Their expansion continued steadily, concluding with a January 2016 decision to make Netflix available in 130 countries overnight (compared to its previous market of roughly 60). Today, it’s available everywhere except China, Syria, North Korea, and Crimea.

Which doesn’t mean the same Netflix experience is available in all of these countries. Netflix’s library varies in size; this site puts their US content library at 4,035 movies and 1,844 TV shows, while Georgia has the smallest library with 1,388 movies and 728 shows.

International expansion gives Netflix a way to amortize the cost of English-language originals across a wider audience–there are 1.0bn English speakers outside of the US. It also gives Netflix a source for new content that can be subtitled, dubbed, or remade in English. But it does impose some costs. Netflix needs local content for each market it cares to expand into, and is often competing against local operators with a better understanding of what audiences want. A recent flop in Nigeria, where Netflix made a sequel to a popular local movie and got a 17% audience score from Rotten Tomatoes, showcases the problem. Movies are hard, and “nobody knows anything”, but it’s an expensive kind of ignorance.

Part of the Netflix model, using quants to match the audience with an auteur, requires a heavy initial investment in content to start generating signals. And the later Netflix starts expanding into a new market, the more catching up it has to do. Meanwhile, other streaming services are setting up their strategy partly around the idea that holding on to users while Netflix catches up to them is easier than growing in line with Netflix. So Netflix is generally bidding for content in a market where the price of content is rising; the mistakes are more expensive (and because some of that expense is to hire famous actors, they’re also more visible).

And that’s just the content side. When Netflix did its massive global rollout, it didn’t quite do local launches: instead, it made an international version of Netflix available in more places. Netflix Russia added local payment options in late 2020, for example, four years after the service became available there. In Brazil, Netflix had to give away equipment to telecoms to ensure that users had enough bandwidth to stream content. 23 of the 38 OECD countries have more than one mobile broadband subscription per capita, but average fixed broadband penetration among them is 33.8%, up only marginally from 28.4% around when Netflix officially went global. So the company benefits from a tailwind of infrastructure investment, but also faces a lower maximum penetration rate outside of the richest developed countries.

Linguistic, cultural, and technological convergence are a long-term tailwind for Netflix. The marginal cost of English-language content that appeals to a broad audience and can be viewed on a smartphone or tablet will keep going down as each of those traits benefits from larger economies of scale. And these are trends that Netflix not only benefits from but accelerates; watching American TV is a classic way to learn English (Neal Stephenson claimed in 1999 that arrestees around the world were asking to be read their Miranda rights; apparently the State Department is not as good at spreading respect for human rights as the Law and Order franchise). Mobile penetration keeps ticking up, and as more video gets consumed on those screens, content gets either mobile-optimized or at least screen size-agnostic. The TV-centered living room may be a development stage that most countries end up skipping, just like many developing countries mostly skip credit cards and go straight to mobile payments. And every incremental device is one more screen that can acquire or retain a Netflix subscriber.

Conclusion

There have been well-articulated bear cases on Netflix since the beginning. When it sold DVDs, it was going to get destroyed by Amazon; when it did rentals, Blockbuster was going to crush it; if Blockbuster didn’t kill Netflix, the company would die by suicide during the Qwikster debacle. In another example of Netflix violating good short-selling heuristics, its CEO argued with a short seller about why Netflix was, if not a buy, at least not a short.[x] Now it’s threatened by well-funded competitors, some of whom, like HBO/Discovery and Disney, have ample content libraries, and others like Amazon and Apple whose customer lifetime value calculations make Netflix’s look tame.

But scale is hard to argue with, and we can work backwards from there. Streaming is a natural transition from linear television; given the opportunity, people will watch a lot of video content in an average day, and given an abundance of choices they’ll pick whatever kind is most appealing to them. Netflix has a lower cost per subscriber given its scale, and while “subscribers” are not perfectly commensurable, Netflix makes them more so over time. Viewers in the US, France, and Germany were all talking about a Korean dystopia last year, and the year before that they were talking about the ludicrously hyper-American Tiger King.

No major technology had a faster path to near-universal adoption than TV, and people don’t revert from on-demand back to linear. While it’s true that other companies have compelling streaming offerings, it’s also true that it takes multiple streaming subscriptions to approach the size of a typical US cable bill. Streaming maximalists who insist on Netflix and HBO and Paramount+ and Disney+ and ESPN+ and so on can eventually top the cost of a giant cable package, but those cable bundles were also the result of cross-subsidization that doesn’t apply in more à la carte consumer choices. The likely steady state is that in the long run, consumers will pay a bit more for data plus streaming content than they did for cable, since they can get the exact bundle they want. And in that world, Netflix won’t necessarily be everyone’s #1 choice—all it really needs to survive is to be a near-universal top three. This might actually be a bit demoralizing for Netflix employees; the company set out to revolutionize an industry, but the industry eventually woke up and revolutionized itself. But while that happened, Netflix converged enough with its suppliers-turned-competitors. The question a few years ago was whether Netflix could turn into HBO before HBO turned into Netflix, and once you’re comparing two HBO-Netflix hybrids, the long-term differentiator is scale.

Disclosure: One of the authors (Byrne) owns shares of Peloton, which was mentioned in this piece.

[x] One thing to notice about Reed Hastings is that he has a penchant for maximizing efficiency and has roughly zero tolerance for wasting time. When analysts get excited about a metric that Netflix has decided is not an important one, he’ll shut them down. This directness comes through in lots of ways: in their corporate communications, Netflix is one of the few companies not to open an earnings call with the CEO and CFO reading a prepared text. Instead, they use the miracle of asynchronous communication–i.e. writing down the prepared remarks and putting them on the Netflix IR page–so the quarterly call can consist entirely of Q&A.

Another example of this, from earlier in the company’s existence: when Netflix first started, it was more successful at selling DVDs than renting them. (The reasons for this are beyond the scope of this footnote, but basically the company took a while to discover that it was better to charge by month than by rental.) At one point, they had a meeting with Amazon to assess Amazon’s interest in buying them–it was assumed that Amazon would get into DVD sales soon enough. The meeting started with Netflix co-founder Marc Randolph swapping stories with Jeff Bezos, until Hastings got bored and insisted that they both get to the point. An interesting conversational gambit for the biggest investor in a company that was negotiating with a bigger, better-funded firm deciding whether or not to crush them.

[x] Interestingly, when they stopped disclosing churn in late 2011, the numbers were looking much worse; domestic churn was 6.3% in Q3 of 2011. Usually, when a metric gets worse and a company stops disclosing it, this is viewed as a bad sign. In Netflix’s defense, they flagged this disclosure change a year in advance, when churn was still improving. Also in their defense, it’s entirely possible that Netflix singlehandedly destroys the backtest for the “short companies that stop reporting a metric as it gets worse” strategy, since their annualized return since they stopped reporting churn is 43%.

[x] A timely detail here is that part of the short thesis on Netflix was that they’d just lost their CFO, Barry McCarthy. From the response: “Barry McCarthy is a very accomplished executive who was working for a successful, younger CEO, so he correctly figured the chances of him becoming the CEO of Netflix were not high. In early 2004 he had the same feeling, and let us know that we should launch a search to replace him by the end of 2004. During that year we entered into a huge fight with Blockbuster (BBI), and Barry felt it would be low integrity to leave us in the midst of battle. So, he agreed to stay for a few more years… Barry is a super-principled guy, and if there were any known major danger, he would never have left us. It is precisely because things look so good going forward that he allows himself to think about his own career ambitions. Some lucky firm will get him as CEO.” McCarthy went on to be CFO of Spotify, then retired, and then came out of retirement to run Peloton last week. “Some lucky firm” is a stale endorsement at this point, but it’s from a reliable source.

Ideas and Apps to

Thrive in the AI Age

The essential toolkit for those shaping the future

"This might be the best value you

can get from an AI subscription."

- Jay S.

Join 100,000+ leaders, builders, and innovators

Email address

Already have an account? Sign in

What is included in a subscription?

Daily insights from AI pioneers + early access to powerful AI tools

Front-row access to the future of AI

Front-row access to the future of AI

Ideas and Apps to

Thrive in the AI Age

The essential toolkit for those shaping the future

"This might be the best value you

can get from an AI subscription."

- Jay S.

Join 100,000+ leaders, builders, and innovators

Email address

Already have an account? Sign in

What is included in a subscription?

Daily insights from AI pioneers + early access to powerful AI tools

Front-row access to the future of AI

Evan Armstrong

Evan Armstrong

Comments

Don't have an account? Sign up!