Evan Armstrong was a lead writer at Every who explored profit and power in technology in Napkin Math.

iBuy, iRent, iLose My Investors Money

The Murky Future of American Housing

Nov 19, 2021 · 12 min readUpdated Jul 22, 2026

Sponsored By: MasterWorks

WSJ: Art is Among the Hottest Markets on Earth

The global wealth of billionaires soared 70% in the last 19 months, and they know exactly what they want: more art. A lot more. Take Jeff Bezos—he spent $70 million last year on two paintings alone.

Billionaires have almost unlimited access to stocks, homes and private equity, but their art holdings could have the biggest payday, market watchers say.

WSJ declared “art is among the hottest markets on Earth.” High-quality works are selling for 15x their asking prices. By 2026, the global value of art is expected to grow by $1 trillion according to Deloitte. And, art has almost no correlation to public equities

Now you can gain exposure to the lucrative art market with Masterworks.io just like me! Their tech platform, recently valued at over $1B, lets you invest in multimillion-dollar paintings by Warhol, Picasso, and Banksy through fractionalized shares just like buying stock in companies.

The best part? Napkin Math Subscribers get priority access*

*See important disclosures.

This year, I watched my friend flip a 13-year-old townhome for a $300k profit after holding it for 3 years. Frankly, the place was a piece of trash. Despite being located in a part of Salt Lake where the best restaurant is Applebees, the house sold within a week or two of being listed. Meanwhile, Salt Lake has had a record 26% home price appreciation just this year. Utah isn’t alone in this dynamic with single family housing across the nation rising ~20%. People searching for a home are unsurprisingly frustrated.

Adding to this craziness is a wave of new, well-capitalized large institutions going after the single family residence home market. Zillow, Opendoor, Blackstone, Blackrock, Builders, REITs, iBuyers, etc, etc, etc. All of them are burning billions trying to change what home ownership means in America.

There is blood in the water.

To explore who wins this race, I’ve teamed up with Marc Rubinstein, the writer of Net Interest. The N of people on the planet who have interesting ideas and can actually write about them is tiny. In the niche world of business analysis, the number is even smaller. The amount of people who can do it every week in public? <50. Marc is one of those people. He writes about the financial sector and is one of the select newsletters where I read every issue. If you like Napkin Math, you’ll like Net Interest.

To understand the battleground of these companies, first we will examine why the US residential market is so dynamic right now. Then we will compare the models of Opendoor (short term flip) versus Blackstone’s Invitation Homes (long term hold) to see what truths we can gleam for their competitive friction. Housing is the single largest investment the majority of people will ever make—it is worth studying closely.

A White Picket Fence and A Fat Contribution Margin

The first thing of note with the U.S. housing market is that is stupid huge. Zillow (who before their collapse we would’ve taken as having best in class data/analysis) estimates that the housing market is $36 Trillion. It is a TAM so large that it boggles the mind to consider. Usually, we see a new startup going after a $10B market we would consider that sufficient so the companies in this market are not starved for land to capture.

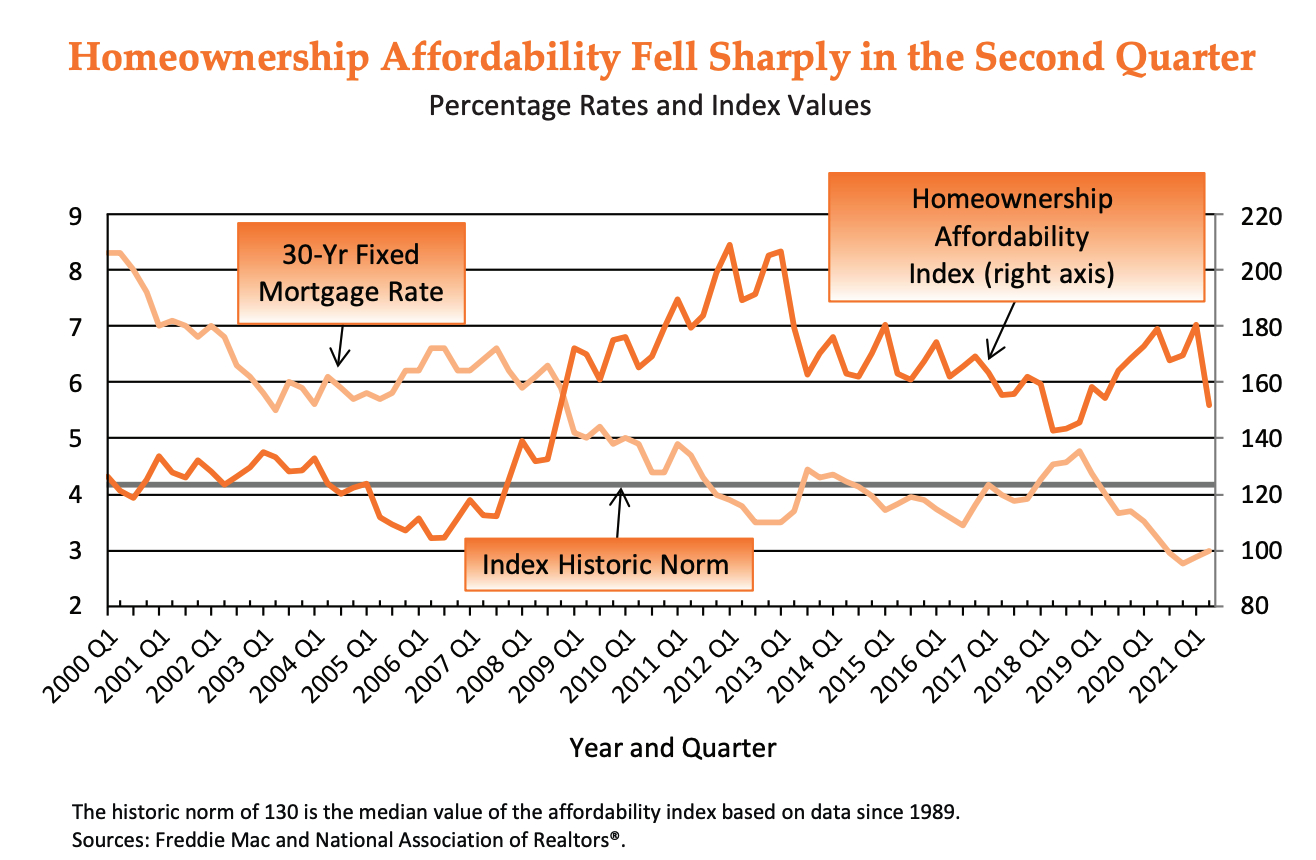

That being said, it isn't exactly going well in U.S. housing. Affordability is sinking ever lower:

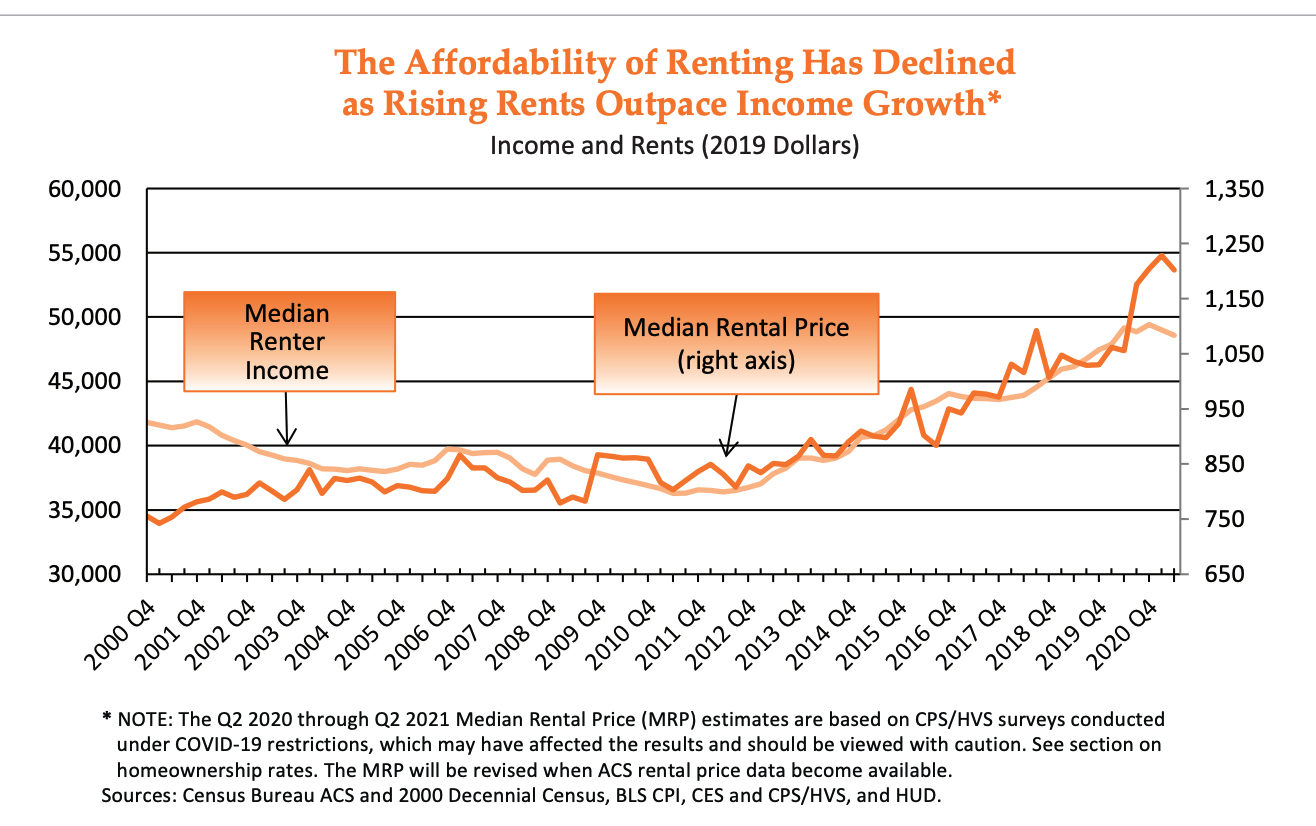

Rental prices continue to go up and up and up:

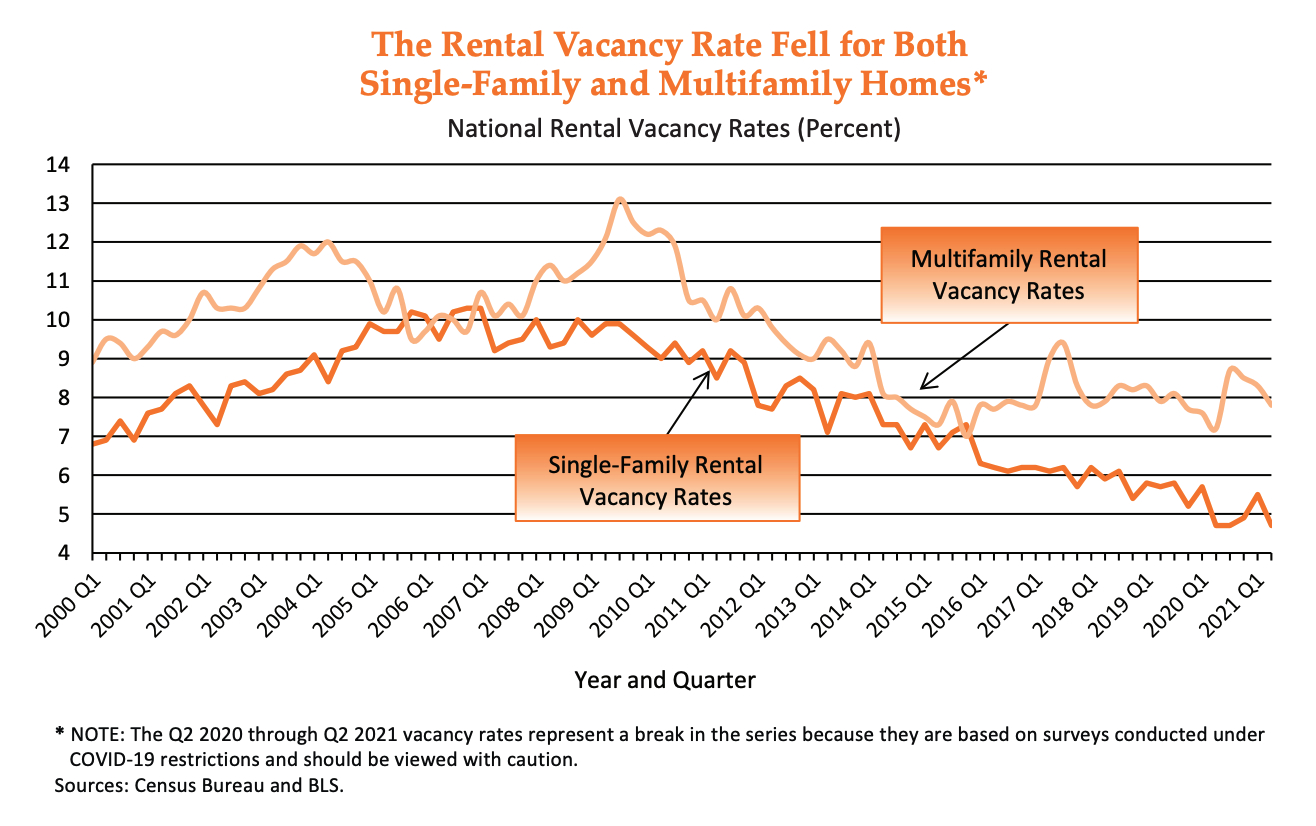

Despite rapidly escalating prices everywhere, vacancy continues to plummet:

You can blame NIMBYs, you can blame local zoning laws, you can blame shortsighted immigration laws decreasing skilled trade labor, shoot, you can blame the cycles of the moon for all we care—it doesn’t matter. This is the reality. Houses and rents are rapidly increasing and there is ever less supply in the market.

Maybe market isn’t actually the right word though. Don't think of Single Family Residential (SFR) as a market but instead think of it as an asset class. Firms like Opendoor and Blackstone are hedge funds engaging in a game of “monetize the housing asset”. The two axes of competition are around how companies source the asset and how they monetize it.

It is additionally important to note that all of these relationships are more frenemies then they are cutthroat competitors. Opendoor will buy homes from Lennar. Lennar will try partnerships with firms like BB living to compete with Blackstone's Invitation Homes. Again, the market is so huge that there is room for everyone.

All of these businesses exist because there is an opportunity for profit (the whole point of the whole capitalism thing) but the customer's reason is that the American housing experience is terrible. Any real estate transaction involves dozens of intermediaries, interactions with local ordinances, and other bureaucratically expensive headaches. Both Opendoor and Invitation Homes are examples of companies trying to simplify the transaction process.

Opendoor’s Cohort Homes

Opendoor is the firm that has most popularized the iBuying experience. Customers go to their website, enter their home address, and Opendoor will tell them how much they will buy their home for at a 5% fee. Using their homegrown algorithm which takes into account neighborhood density, refurbishment needed, and dozens of other data points, they are able to (hopefully) give the owners a price that allows Opendoor to make money on the other side when they sell the house over the next few months.

Following the transaction, Opendoor will sometimes add light upgrades like new paint and carpet, and then sell the house. Using this process, last quarter Opendoor acquired ~15K homes spread across 44 markets and sold roughly 5K. All of this effort resulted in a 6-9% commission rate. The average contribution margin was 7.5% last quarter that came from home price appreciation and an increase in higher margin services.

The model powering the numbers is a business of bundles.

The first bundle is around the bundled housing assets. Homes are large cash volume purchases and the margin for error is very slim. If Carvana misprices the cars it purchases by 5% it is only a swing of a few thousand dollars per unit and they can easily make it up with other vehicles. If Opendoor does it, a 5% swing in a $500K home is a $25K difference. If you are to purchase 100 homes, and have a 5% misprice on of the homes with a 500K average selling price you are looking at $125K in loss over the bundle. To make it even more difficult, your error will only be obvious at the end. Let’s say you buy 100 homes on Day 1, the correctly priced assets will flip relatively quickly. Day 30 the great stuff is gone, Day 60 the good stuff is gone, and by Day 120 all you are left with is the bad apples. Note: This is part of why the Zillow shut down felt so sudden. Zillow thought they were geniuses until suddenly they weren’t.

The second bundle dynamic is the services that you can bundle together to eke out more margin per customer. Things like moving services and loans will help raise the transaction per home margin and dollar volume. Typically when we hear the “we just need to sell more things to the same customers and then we will be profitable” story our tendency is to roll our eyes. It is just really hard to increase the share of wallet for businesses. However, Opendoor has positive tailwinds—buying a house sucks. There are so many associated pain points that desperately cry out for vertical integration that this opportunity is for Opendoor’s to lose.

As an example, consider Opendoor’s newest product—Opendoor Complete. One of the most frustrating aspects of house hunting is the double mortgage. Timing the purchase of a new home and the sale of your old one is terrible. Complete allows for individuals to secure an offer from Opendoor for their current home, then take their time in finding the next house. They can select the date the transaction will occur and when they will move. This is wildly easy in comparison to the labyrinth of choices. Software automating bureaucracy is amazing.

Nevertheless, good solutions do not always make good businesses. The capital required is enormous. Opendoor finances their purchases with mostly debt. They have yet to consistently produce positive cash flow, be EBITDA positive, or show that their purchasing algorithm can suffer in a market with high headwinds.

If you are convinced that SFR will continue to be an attractive market but are unconvinced by the Opendoor model, Invitations Homes offers a monetization model that focuses on the long term cash flow versus the quick flip of Opendoor.

An Invitation Home

Opendoor and the other iBuying firms are relatively new players in the huge residential real estate market. Arguably, their route into the market was eased by another group: institutional owners of single family rental homes. The biggest player in this group is Invitation Homes.

Up until about ten years ago, most rental homes in the US belonged to individuals or mom-and-pop outfits. Renting homes was a hyper-local business; it was very capital intensive and it didn’t exhibit obvious economies of scale. But in the aftermath of the financial crisis, home prices fell to levels that attracted the attention of institutional investors. One of them was Blackstone. Foreclosed homes were being auctioned off on courtroom steps all over the country, in many cases at prices below their replacement cost, and Blackstone decided to dip in. In spring 2012, the firm paid $100,000 for its first purchase, a house in Phoenix. Within a few months, it was buying $125 million worth of homes every week.

Blackstone’s insight wasn’t just that these were cheap assets, it was that there was an opportunity to institutionalize the process of buying and renting homes. The firm created a platform – Invitation Homes – and invested in processes to buy, renovate, lease, maintain and manage homes efficiently and at scale. On the buying side, that meant modeling tons of market data around factors like neighborhood desirability, proximity to local amenities, construction type, ongoing capital needs and so on. Before it had bought its 50,000th home, Invitation Homes had analyzed data on over a million.

Invitation Homes deployed processes to make maintenance and management of homes more efficient, too. But it’s the buying process that paved the way for Opendoor and the others. If Invitation Homes could use technology to source acquisitions for its buy-and-hold strategy, why couldn’t others do the same for buy-and-sell? One analyst, Byrne Hobart, has even suggested that the inflow of institutional capital from firms like Invitation Homes altered market dynamics, introducing more short-term volatility and less momentum into home prices, creating a more conducive market for the iBuyer model. Invitation Homes may have agreed. In March 2018, it invested $10 million in Opendoor’s series E funding round. It also uses iBuyers as an acquisition channel for its homes now that its days on the courtroom steps are over. According to one statistic, institutional buyers make up over 9% of iBuyer sales.

Although both iBuyers and institutional rental platforms rely on an extensive use of data to inform their home-buying decisions, their models are calibrated very differently. That’s because while one group makes its money from gains on sale, the other makes it off income. Invitation Homes makes occasional property sales but they’re not a core focus. Rather, the company budgets for homes remaining on its balance sheet for many years. It can afford to practice the Warren Buffett school of asset acquisition – “it’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price” – a luxury not available to the gain-on-sale investor.

Today, Invitation Homes owns over 80,000 homes in 16 markets across the United States. The company’s buying decisions are driven by rental yield – if it can deploy capital at yields greater than its cost of capital, it’ll go for it. So far this year, it has acquired 1,977 new homes at rental yields in excess of 5%. Increasingly, a lot of its acquisitions are being sourced directly from homebuilders – up to around a fifth – and the company has agreed a pipeline with Pulte Homes which will start delivering next year.

Average occupancy of its homes is currently 97%, with the company pulling in around $2,000 in rent per occupied home per month. It’s pretty fashionable these days to refer to a business as a subscription business, and Invitation Homes is no exception. The company’s customers “value the convenience of a worry-free subscription-based lifestyle,” said the CEO on his latest earnings call. That means managing churn. Annual turnover is currently around 25% but, unlike a subscription business, churn is not all bad. On the one hand, it leaves properties unoccupied – typically for around 25 days – and therefore non-income generating. But on the other hand, it presents an opportunity to write a new lease. Right now, new leases are being written at 18% higher rents over the previous quarter; that compares with renewal leases (where the resident stays) which are up around 8%.

Maintaining a portfolio of 80,000 homes is not cheap, but Invitation Homes is able to extract some efficiencies from its scale. It manages its portfolio as a series of ‘pods’, looked after by teams of 10-12 people with supporting maintenance staff on the ground. As the company has grown, the number of homes per pod has increased from around 1,500 to around 3,000. Further efficiencies come from procurement – cheaper flooring, smart home technology and the like. All-in, the operating margin in the business is around 57%.

The big drag is the same one Opendoor faces: it’s a capital intensive business. The homes sit on Invitation Homes’ balance sheet at a valuation of $16.6 billion. They are financed roughly 50/50 between debt and equity. Equity holders have had the benefit of some considerable home price appreciation, of course. That first property in Phoenix is worth a fair bit more than $100,000 today. But the model doesn’t depend on home price appreciation. Contrast that with Opendoor, which had around $6.3 billion of inventory on its balance sheet at the end of the quarter – a big number, but one that turns over more quickly, allowing for a 75/25 split between debt and equity.

A New Market Structure

The residential real estate market is huge and feeds a vibrant ecosystem of business models: realtors, appraisers, title insurers, mortgage originators, mortgage servicers, the list goes on. Historically it has been a very fragmented industry, built around local knowledge. There are 95 million homes in the US, no two identical. But in the past ten years, two things have changed; possibly three.

First, many of the houses built in the boom years before the financial crisis do look the same. Indeed, this may have exacerbated the downturn in home prices during the crisis as contagion spread within ZIP codes. Some markets have therefore become more homogeneous.

Second, technology has enabled market participants to model house prices more effectively. Opendoor talks about using 100 data points per home; at the time of its IPO, Invitation Homes talked about 64 factors. Of course, no pricing model can capture the vagaries of human behaviour, particularly around as personal an asset as housing, but compared to what existed before, this is a big improvement.

Both of these factors make residential housing more tradeable than it was, which impacts market structure. (The third shift is low interest rates, which may have contributed to institutional demand for yield, but keep asking why and you’ll always come back to low interest rates.)

Against that backdrop, a role for market makers like Opendoor and institutional buy-and-hold capital like Invitation Homes has emerged. Currently, they have a small share of the overall market, even in the more homogeneous markets where they are both active. But as marginal buyers they have a big impact. A fragmented market may be less efficient, but no player is large enough to influence the market price. Inject more institutional capital into a market and that can change. Those charts up top? That may be what happens when whales enter a market.

Sponsored By: MasterWorks

Thanks again to our sponsor, MasterWorks.

If you want to get portfolio exposure to the art market without needing to spend hundreds of thousands or millions of dollars, I highly recommend you check them out and get priority access:

The Only Subscription

You Need to

Stay at the

Edge of AI

The essential toolkit for those shaping the future

"This might be the best value you

can get from an AI subscription."

- Jay S.

Comments