Sponsored By: Fundrise

You don’t have to be IN real estate to invest in it. Fundrise is an easy-to-use platform that lets you build, grow and manage a diversified portfolio of high-end private real estate projects across the US. These are the same types of investments that power the largest pension funds, endowments, and sovereign wealth funds.

Fundrise offers significantly deeper diversification and outsized performance potential — a true alternative to any public market asset. They have become America’s largest direct-to-investor real estate platform by digitizing, automating, and integrating almost every aspect of the private investment industry in order to maximize your long-term return potential.

With Fundrise, you can achieve true portfolio diversification at the touch of a button. Find out how 210,000+ investors from all sizes are diversifying their portfolios with our private real estate investments.

I’m excited to have a guest post today from Kyle Harrison. In the past, he’s worked at firms like Coatue and Index Ventures, and for the last few months has been writing about the rapidly evolving VC landscape at Investing 101. Today he’s going to dive into the examples he’s seen of when cash is a king maker and when it's a kiss of death.

What's In a Moat?

For the last few years in startupland, cash was a commodity. Startups were stuffed full of capital from family offices, hedge funds, and me and other people like me in venture capital. Now however, the paradigm has shifted. Cash is more difficult to raise and the world is increasingly giving 2001 popped tech bubble vibes. If this apocalypse comes to pass, investment dollars will become more scarce. Cash will cease to be a commodity. The key question that all entrepreneurs and investors must ask is when does cash become a competitive advantage?

Everyone loves to talk about moats in business. Are they defensible? Are they differentiated? One heated debate is around whether a moat can consist of cash. However, it isn’t just whether or not it is a “moat” but whether it’s defensible. Does that cash allow a firm to maintain market share and profits?

In building a business there are no sure bets. You can have the most tenured executives, the most advanced technology, the strongest tailwinds, and the most direct access to capital and still fail. You can also have little more than an idea and a computer but still be wildly successful. Cash can only ever be a part of the equation.

When you look at a number of case studies in industries that have sucked up a lot of the venture cash floating around you see some insightful patterns. The advantage a business can get from having a huge amount of cash typically has more to do with the underlying market dynamics, maturity, and user economics, than it does with the cash itself. In other words? All cash-spending activities don't create equal results.

There is a common thread across industries that have come up as I've dug into the cash habits of the rich and the famous (companies). The first is a mindset. Some of the companies that have used cash most effectively have had a particular mindset while the ones who most abused cash had a very different perspective. The second is a focus on particular metrics. When thinking through how much of an advantage cash can provide there are some key metrics that can be most telling. Once you understand the mindset and the metrics around cash we can walk through case studies like Uber or Snowflake and better understand the way these companies have operated. Up first? Mindset.

A Paranoid Abundance Mindset

Your attitude towards money will always have more impact than how much money you actually have. For better or for worse. One of the most opulent examples of a cash inferno mindset is WeWork. A company that stands basically alone in having its downfall come from nothing other than simply filing an S-1 and letting the public look under the hood.

If you don't remember the fall of WeWork very well you might be thinking, "wait, didn't COVID have something to do with it?" Insanely enough? No. WeWork released their S-1 to a gobsmacked public in August 2019 after having raised over $12B in funding and seeing their valuation skyrocket to $47B. Things unraveled pretty quickly after that. The CEO stepped down in September, SoftBank took control of the company in October, and WeWork laid off 2,400 people in November. Today? WeWork is finally a public company trading at ~$5B.

What was the behavior that so shocked the world and led to one of the biggest unravelings a company has seen? An insane attitude towards spending, burning $2B a year in cash, pointing to their widely-ridiculed "community-adjusted EBITDA profitability," and the CEO claiming “energy and spirituality” as more relevant metrics for its potential in public markets than measures of its revenue and losses.

A more recent example is Fast. In November 2020, when Fast was roughly 18 months old they were raising opportunistic rounds far ahead of product-market fit because they believed they could "close a round on favorable terms due to conditions in the VC market." That opportunistic attitude was the driver behind bringing on more cash, regardless of the product or customer demand. That round eventually came together when Stripe led a $102M Series B in January 2021.

That cash-induced confidence pushed Fast to grow their headcount to ~500 people leading to a cash burn of $10M per month. At revenue of ~$600K that was $1,200 per employee. In a stream of cash-incinerating activities you hear about $90K events thrown in Tampa, corporate retreats in Honolulu and Denver, and corporate coaches flown in who work with professional athletes. All of this is indicative of a mindset that is filled with abundance and lacking any paranoia.

Any company can have a plan for how they approach their spending habits. But the public markets can often stand in for Mike Tyson. "Everyone has a plan until they get punched in the face." Developing a strategic mindset around how you spend cash isn't a function of simple frugality. The mindset is meant to help with maintaining scrappiness and leveraging cash in the most effective way possible. So how can you measure how effective you've been with your cash?

Some of the most effective managers of cash seem to have found the perfect balance in their mentality between paranoia and abundance. The market correction of the last few months has reminded a lot of people why paranoia is a necessary ingredient. We're not talking about just being a penny-pincher and hoarding cash under a mattress. The most effective operators understand cash is a weapon that needs to be used effectively. There are some key metrics that cut through the noise and help identify the most effective spending habits.

Metrics That Matter

For financial nerds there is a lot to love when looking at a company's P&L. But the sexiest thing about a company isn't the size of its revenue or even its growth rate. It's the cash conversion cycle! How effectively does a company turn cash into more cash? This isn't only how effectively you manage operations or how high your margins are. It's also optimizing your business model to most effectively finance your operations.

Jay Vasantharajah laid out a great example using Gymshark's financials. They have a negative cash conversion cycle. "A negative cash conversion cycle means that your vendors finance your operations and no extra cash needs to be invested as you grow."

The reason cash conversion is so fascinating and powerful is because it is actually a pretty effective way to compare businesses apples to apples. If the ultimate purpose of a business is to eventually generate reliable streams of cash flow, then how effectively the business takes in cash and turns it into more cash is a key question to ask.

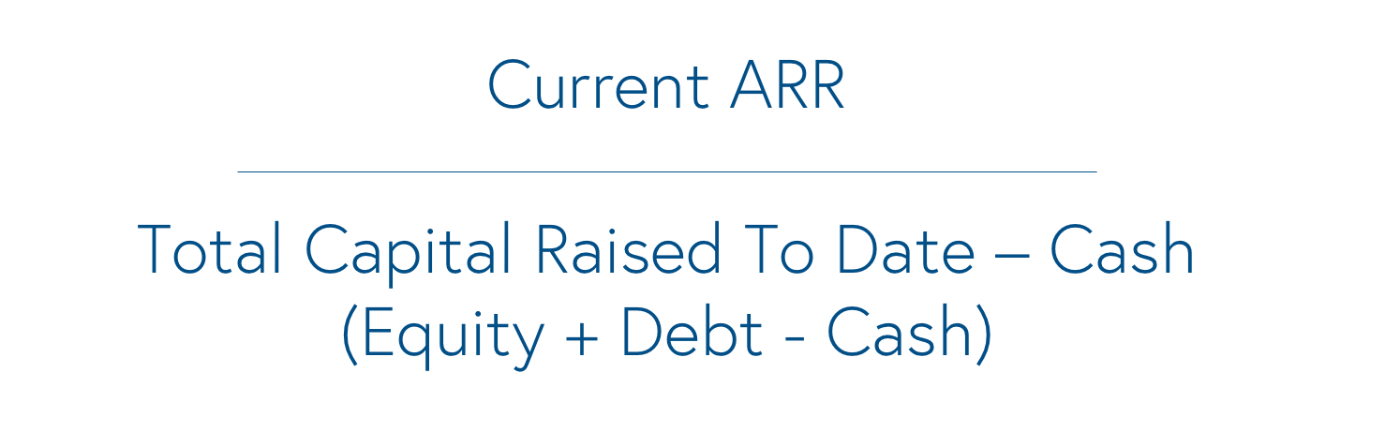

Bessemer has done a great job explaining the concept of cash conversion for cloud software companies. Their straightforward calculation is a proxy for ARR created for every dollar of cash burned.

Sponsored By: Fundrise

You don’t have to be IN real estate to invest in it. Fundrise is an easy-to-use platform that lets you build, grow and manage a diversified portfolio of high-end private real estate projects across the US. These are the same types of investments that power the largest pension funds, endowments, and sovereign wealth funds.

Fundrise offers significantly deeper diversification and outsized performance potential — a true alternative to any public market asset. They have become America’s largest direct-to-investor real estate platform by digitizing, automating, and integrating almost every aspect of the private investment industry in order to maximize your long-term return potential.

With Fundrise, you can achieve true portfolio diversification at the touch of a button. Find out how 210,000+ investors from all sizes are diversifying their portfolios with our private real estate investments.

I’m excited to have a guest post today from Kyle Harrison. In the past, he’s worked at firms like Coatue and Index Ventures, and for the last few months has been writing about the rapidly evolving VC landscape at Investing 101. Today he’s going to dive into the examples he’s seen of when cash is a king maker and when it's a kiss of death.

What's In a Moat?

For the last few years in startupland, cash was a commodity. Startups were stuffed full of capital from family offices, hedge funds, and me and other people like me in venture capital. Now however, the paradigm has shifted. Cash is more difficult to raise and the world is increasingly giving 2001 popped tech bubble vibes. If this apocalypse comes to pass, investment dollars will become more scarce. Cash will cease to be a commodity. The key question that all entrepreneurs and investors must ask is when does cash become a competitive advantage?

Everyone loves to talk about moats in business. Are they defensible? Are they differentiated? One heated debate is around whether a moat can consist of cash. However, it isn’t just whether or not it is a “moat” but whether it’s defensible. Does that cash allow a firm to maintain market share and profits?

In building a business there are no sure bets. You can have the most tenured executives, the most advanced technology, the strongest tailwinds, and the most direct access to capital and still fail. You can also have little more than an idea and a computer but still be wildly successful. Cash can only ever be a part of the equation.

When you look at a number of case studies in industries that have sucked up a lot of the venture cash floating around you see some insightful patterns. The advantage a business can get from having a huge amount of cash typically has more to do with the underlying market dynamics, maturity, and user economics, than it does with the cash itself. In other words? All cash-spending activities don't create equal results.

There is a common thread across industries that have come up as I've dug into the cash habits of the rich and the famous (companies). The first is a mindset. Some of the companies that have used cash most effectively have had a particular mindset while the ones who most abused cash had a very different perspective. The second is a focus on particular metrics. When thinking through how much of an advantage cash can provide there are some key metrics that can be most telling. Once you understand the mindset and the metrics around cash we can walk through case studies like Uber or Snowflake and better understand the way these companies have operated. Up first? Mindset.

A Paranoid Abundance Mindset

Your attitude towards money will always have more impact than how much money you actually have. For better or for worse. One of the most opulent examples of a cash inferno mindset is WeWork. A company that stands basically alone in having its downfall come from nothing other than simply filing an S-1 and letting the public look under the hood.

If you don't remember the fall of WeWork very well you might be thinking, "wait, didn't COVID have something to do with it?" Insanely enough? No. WeWork released their S-1 to a gobsmacked public in August 2019 after having raised over $12B in funding and seeing their valuation skyrocket to $47B. Things unraveled pretty quickly after that. The CEO stepped down in September, SoftBank took control of the company in October, and WeWork laid off 2,400 people in November. Today? WeWork is finally a public company trading at ~$5B.

What was the behavior that so shocked the world and led to one of the biggest unravelings a company has seen? An insane attitude towards spending, burning $2B a year in cash, pointing to their widely-ridiculed "community-adjusted EBITDA profitability," and the CEO claiming “energy and spirituality” as more relevant metrics for its potential in public markets than measures of its revenue and losses.

A more recent example is Fast. In November 2020, when Fast was roughly 18 months old they were raising opportunistic rounds far ahead of product-market fit because they believed they could "close a round on favorable terms due to conditions in the VC market." That opportunistic attitude was the driver behind bringing on more cash, regardless of the product or customer demand. That round eventually came together when Stripe led a $102M Series B in January 2021.

That cash-induced confidence pushed Fast to grow their headcount to ~500 people leading to a cash burn of $10M per month. At revenue of ~$600K that was $1,200 per employee. In a stream of cash-incinerating activities you hear about $90K events thrown in Tampa, corporate retreats in Honolulu and Denver, and corporate coaches flown in who work with professional athletes. All of this is indicative of a mindset that is filled with abundance and lacking any paranoia.

Any company can have a plan for how they approach their spending habits. But the public markets can often stand in for Mike Tyson. "Everyone has a plan until they get punched in the face." Developing a strategic mindset around how you spend cash isn't a function of simple frugality. The mindset is meant to help with maintaining scrappiness and leveraging cash in the most effective way possible. So how can you measure how effective you've been with your cash?

Some of the most effective managers of cash seem to have found the perfect balance in their mentality between paranoia and abundance. The market correction of the last few months has reminded a lot of people why paranoia is a necessary ingredient. We're not talking about just being a penny-pincher and hoarding cash under a mattress. The most effective operators understand cash is a weapon that needs to be used effectively. There are some key metrics that cut through the noise and help identify the most effective spending habits.

Metrics That Matter

For financial nerds there is a lot to love when looking at a company's P&L. But the sexiest thing about a company isn't the size of its revenue or even its growth rate. It's the cash conversion cycle! How effectively does a company turn cash into more cash? This isn't only how effectively you manage operations or how high your margins are. It's also optimizing your business model to most effectively finance your operations.

Jay Vasantharajah laid out a great example using Gymshark's financials. They have a negative cash conversion cycle. "A negative cash conversion cycle means that your vendors finance your operations and no extra cash needs to be invested as you grow."

The reason cash conversion is so fascinating and powerful is because it is actually a pretty effective way to compare businesses apples to apples. If the ultimate purpose of a business is to eventually generate reliable streams of cash flow, then how effectively the business takes in cash and turns it into more cash is a key question to ask.

Bessemer has done a great job explaining the concept of cash conversion for cloud software companies. Their straightforward calculation is a proxy for ARR created for every dollar of cash burned.

If a company raised $100M and they have $50M left that means they've burned $50M (give or take, depending on profitability). If they have $25M ARR their cash conversion score is 0.5. But if they have $100M of ARR then their score is 2. The higher the score? The more effective they are at taking cash and converting it into ARR.

Bessemer's research into various company's cash conversion scores points to a pretty clear correlation between effective cash conversion and investment returns. They summarized their key point this way:

“We realize that some might take this data to imply that raising incremental capital is bad, but that is not the takeaway at all. The median public cloud company raised $160MM to get to a ~$100MM revenue scale, with some companies having raised up to $750MM; it takes financing to build a market-leading company. Instead, the takeaway is that the great companies can use the capital raised to catalyze growth. They built their fantastic Cash Conversion Scores not by starving themselves of capital but rather through growing revenue alongside their capital base.”

My focus here isn't to settle the debate on bootstrapped vs. the "grow-at-all-costs" amounts of funding some companies raise. I'm a VC so I'm obviously in the business of encouraging companies to take money when it could make a difference for their outcome. For a lot of businesses that are chasing very large potential outcomes there is an opportunity to leverage cash to win. So let's look at some case studies.

Cash as a Case Study

The evolution of the "cash as a weapon" argument has historically played out when people see a market as "winner-take-all." A lot of these examples historically have been in consumer markets where companies are racing to develop a new behavior (ordering a ride with a stranger or food to your door.) But the addiction to cash spread far and wide during the bull market of the last few years. The key points to focus on here are

- How did players in a particular market treat cash?

- How did cash impact the outcome in the market?

- And most importantly, did those cash habits lead to a lasting competitive moat?

Ride-Sharing

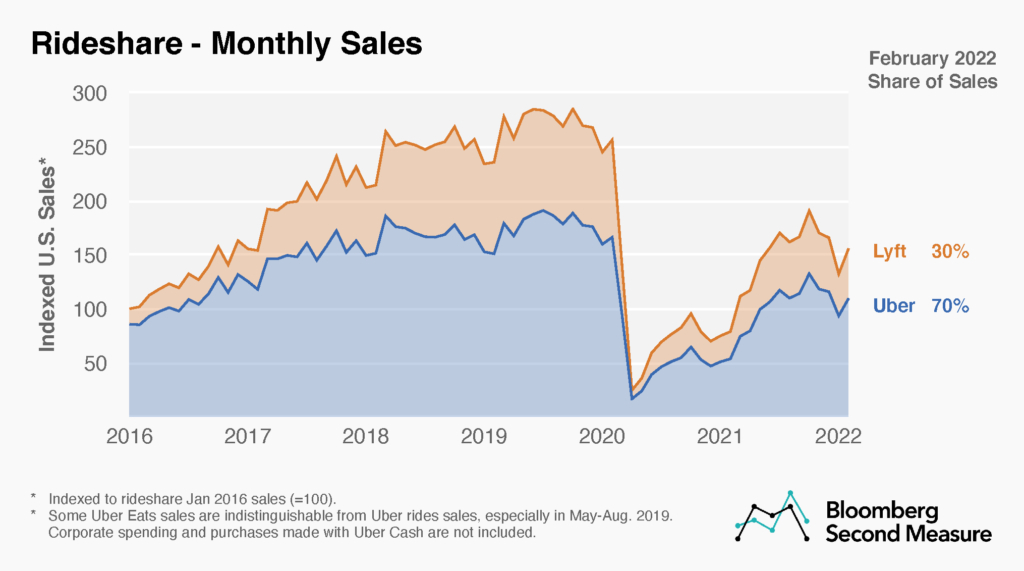

For a lot of people, ride-sharing was one of the original "Cash War" battlegrounds. There were a lot of competitors and the ones that stuck around were the ones that could fundraise most effectively. Uber and Lyft raced to raise more money, to spend more on marketing, to open new markets, and to attract more drivers. Uber focused much more on breadth pushing to cover more international markets more quickly. Cash became what a lot of people saw as a differentiating factor. Back in 2017 SoftBank even used this as a negotiation tactic, effectively telling Uber "either you take our money, or we'll go give it to Lyft."

Fast forward to today, when you look at Uber and Lyft there are plenty of arguments for which is the better business. Just a rough glance at the numbers, it's clear Uber is the larger business with a $68B market cap, $17.5B in revenue, and their first profitable quarter. Lyft is at a $13B market cap with $3.2B in revenue.

And when you look at the history of capital raised the numbers are staggering and the difference is stark. Keep in mind there are only 56 companies in the world that have raised over $5B in venture funding. Uber raised $25B (in debt and equity) while Lyft raised a little over $5B. This isn't a perfect proxy for the ARR to cash burn calculation in Bessemer's conversion score but just as a thought exercise think about this as a conversion.

Uber raised $25B to generate $17.5B in revenue (17.5/25 = 0.70). Lyft raised $5B to generate $3.2B in revenue (3.2/5 = 0.64). Lyft also has operating income margins at -33% vs. -22% for Uber. In the case of Uber vs. Lyft? Cash as a weapon seems to have been an effective strategy. But cash as a long-term lasting moat? Doesn't seem like it. As recently as Uber's earnings call in February 2022 they spent a lot of time talking about strategies to reduce their CAC. If your CAC stays high even as you dominate a market you likely don't have a very effective moat.

Enterprise Software

In software there are two interesting trends that have made it possible to build a company with significantly fewer resources. First, the overall infrastructure cost of building software has gone down. You don't have to rack your own servers, you can just use AWS. And second, the proliferation of things like open source and product-led growth have made it easier than ever to initially distribute software without massive marketing budgets. However, a lot of SaaS businesses are adopting this "winner-take-all" mentality we've seen play out in ride-sharing and food delivery where these companies burn like crazy to capture their respective markets.

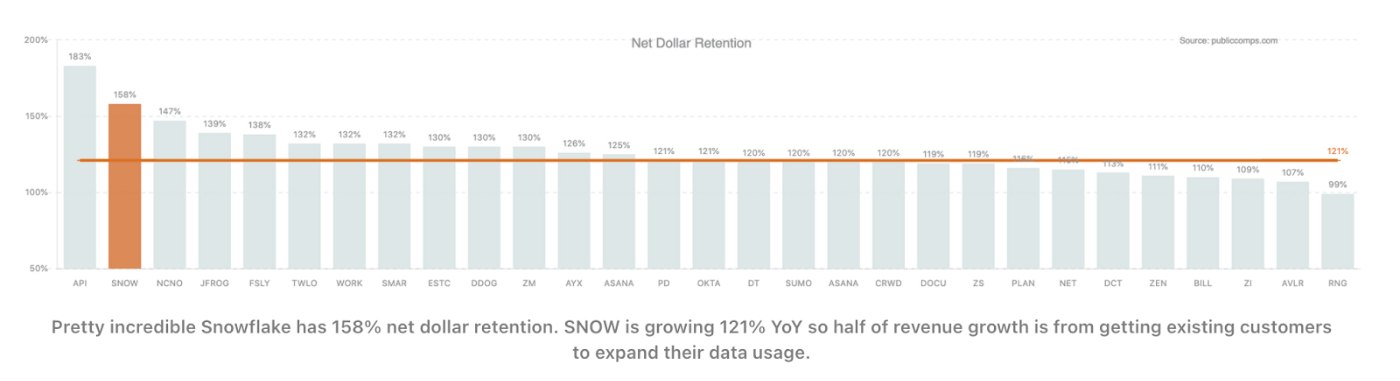

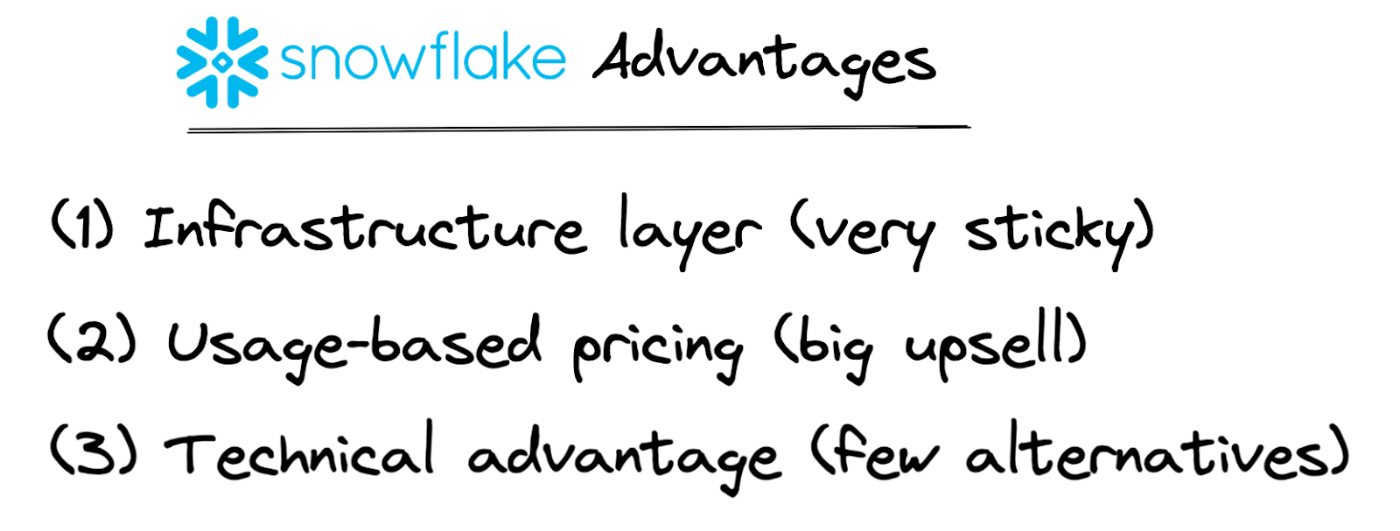

Snowflake is a good example of this. They raised a total of $1.5B in funding and burned nearly $200M in order to get to $100M of ARR. And even then they've always had low gross margins which exacerbates burn (their GM only barely passed 60% last year). In Bessemer's cash conversion score that would barely make the middle bucket. Snowflake's model exposes some key insights into situations where raising large amounts of cash and being willing to burn can make sense.

They can afford to spend $150K to acquire a customer even if they initially only pay $50K. Why? Snowflake is an incredibly sticky product because it sits at the infrastructure level so people will very rarely rip it out. That plus their usage-based pricing model produces net retention at 178% so Snowflake is seeing massive expansion in their customers. That's why Snowflake can afford to spend. They can spend $150K to acquire a customer because within 2 years that customer will typically be 3x in size.

But the lesson here isn't "software is great, go ahead and light money on fire." Snowflake is a unique case with some pretty critical characteristics. The fact that most businesses don't have these characteristics is a big reason why every software company can't and shouldn't trade at a Snowlake-esque multiple.

There are plenty of categories in software that don't enjoy the same advantages. And that's where "cash as a weapon" might get people into trouble.

Productivity Software

There is no category where product-led growth has thrived more effectively than in productivity software. Airtable,, ClickUp, Notion, Coda are examples of recent stalwarts. A lot of people point to this grassroots user awareness and adoption as a moat in itself. Some of these companies think of Jira as an analogy for the ubiquity they hope to achieve. Among developers Jira has a whopping 84% market share.

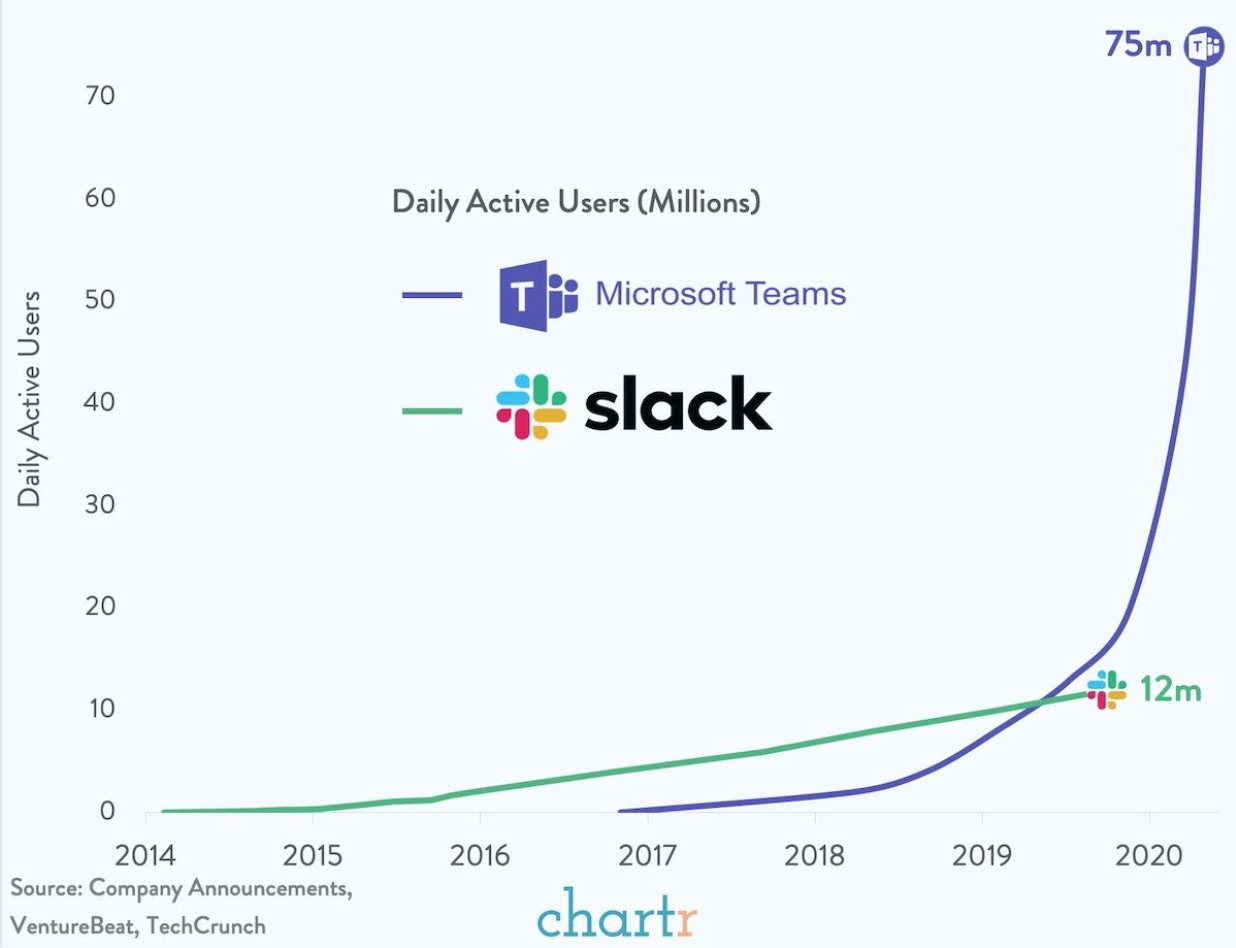

The problem with this idea of ubiquity and grassroots awareness acting as a moat is that it doesn't play out in productivity software. There is very rarely an intense stickiness for application software. When you look at something like Atlassian, they're serving primarily developers who are much more homogenous. They work in very similar ways with very similar tools. Knowledge workers? All over the spectrum. The only reason Microsoft has penetrated knowledge workers so heavily is because they have Windows as an automatic distribution engine. And we've seen that distribution engine play out against an incumbent productivity tool: Teams vs. Slack.

Productivity tools will raise a bunch of money, spend dramatically to increase their awareness and even though they have strong bottom-up momentum it's very similar to Uber or Doordash. Is there market awareness of their product? Sure. More and more. Is it a sustainable moat? As soon as they stop spending on marketing, the next tool will push for more awareness and eat away at their advantage. They're just not inherently sticky, unlike Snowflake. It's fairly unlikely that anyone is using Notion as their core enterprise "system of record" in a way that would make them never rip it out.

When you start to think about all the factors that make a compelling argument for why dramatic amounts of cash burn make sense, the case is much weaker for productivity software than it is for Snowflake.

Differentiation At the App Layer

Quick counter-argument to differentiation at the application layer? Workday. The product that uniformly people will acknowledge is an absolute pain to work with and get right. But guess what? 90% of the Fortune 100 are customers. They have 95% gross revenue retention so just about no one leaves. If you have a software application that looks like Workday then you should spend quickly to sink your teeth deep into the market because no one can ever unseat you.

So... What's in a Moat?

Building a defensible moat is one of the hardest things to do in building a business. You should do yourselves as many favors as possible in finding components of your product or market that lend themselves to establishing natural moats. Cash can help you build any number of those, but it's important to understand when burning to build a moat is the right call.

My analysis of these companies would argue there are 4 reasons to leverage cash to help build a moat:

- Building new behaviors: Uber and DoorDash were pushing to get users to develop new behaviors. If you can own a market and become THE solution people associate with that behavior there could be inherent customer loyalty in that.

- Unit economics at scale: Some companies see their unit economics change at scale. On the consumer side it's DoorDash or GoPuff that are looking for significant user density. On the enterprise side companies like Attentive or Braze that offer SMS marketing have to pay a fee per message delivered. The larger volumes they have the more negotiating power they have with carriers or 3rd parties like Twilio.

- Stickiness: Whether stickiness comes from a technical advantage like Snowflake being embedded infrastructure or just from being so interwoven and complex like Workday that no one will ever want to rip it out. Inherent stickiness is a double edged sword. It can work for you if you get there first, but it will work against you if your competitor is already there.

- Massive expansion: When you know a customer will naturally expand with your product (e.g. more usage with Snowflake or more payments with Stripe) then it makes sense to burn to get into those customers so that you can grow with them.

There are also 4 reasons to be cautious of leveraging cash to build a moat that may not be sustainable:

- Lack of defensibility: The reason application software often struggles to have a meaningful moat is because the differentiation is mostly in the interface. UI is not a long-term competitive advantage.

- No platform advantage: When you talk about a "system of record," you see what most software companies aspire to be. The question is whether you have a viable path to becoming a system of record. Often people point to their access to data as a claim to first becoming a system of intelligence and then replacing the system of record, but we have yet to see an example of that in the real world.

- No distribution advantage: Think of Microsoft being able to use Windows to push Teams. Or Uber being able to launch Eats with their existing driver network. Open source or product-led growth can certainly be distribution advantages but they're rarely a long-term defensible moat because they're available to everyone.

- Limited upsell opportunities: Every company has to have a viable argument to explain why their product can progressively become more important to a company. Companies like Lattice have expanded their NDR from ~100% to 120% over the last year or so as they've added product modules in HR. If you're a point solution you need a clear path to product expansion that leads to revenue expansion in order to justify burning to acquire customers.

There will always be the “move fast and break things” people who want to raise $100M every 6 months lighting money on fire as they go. And there will always be the bootstrapped worriers who look at VCs as parasites who ruin businesses. Neither of them will always be right or wrong. Cash, like any strategic asset, is a double-edged sword. It can be used effectively (even in large quantities) or it can impale you. The difference is whether you're decisive enough to dictate how you use it.

Ideas and Apps to

Thrive in the AI Age

The essential toolkit for those shaping the future

"This might be the best value you

can get from an AI subscription."

- Jay S.

Join 100,000+ leaders, builders, and innovators

Email address

Already have an account? Sign in

What is included in a subscription?

Daily insights from AI pioneers + early access to powerful AI tools

Front-row access to the future of AI

Front-row access to the future of AI

Ideas and Apps to

Thrive in the AI Age

The essential toolkit for those shaping the future

"This might be the best value you

can get from an AI subscription."

- Jay S.

Join 100,000+ leaders, builders, and innovators

Email address

Already have an account? Sign in

What is included in a subscription?

Daily insights from AI pioneers + early access to powerful AI tools

Front-row access to the future of AI

Evan Armstrong

Evan Armstrong

Dan Shipper

Dan Shipper

Comments

Don't have an account? Sign up!