.png)

Sumeet Singh is the founder and managing partner of the venture capital firm Worldbuild.

Two Ways to Win in the Post-software Era

If you're funding or starting an AI company in 2025, Rich Sutton's 'bitter lesson' should terrify and guide you

Dec 8, 2025 · 12 min readUpdated Jul 10, 2026

Sumeet Singh has spent his career placing bets on the future—first as a partner at Andreessen Horowitz, and now as the founder and managing partner of Worldbuild. After eight years of investing and conversations with hundreds of AI founders, he’s noticed a troubling pattern: Most are building specialist AI tools the same way they would have built SaaS products a decade ago. In our latest Thesis, he makes the case that this approach is a trap. Drawing on Richard Sutton‘s “bitter lesson”—the idea that scale and compute always beat specialization—Sumeet maps out the two paths he sees for founders who want to build something durable: Either build what models need to get better, or invent entirely new workflows that only AI makes possible. Read on for his breakdown of both paths, and the question every founder and investor should be asking right now.—Kate Lee

Was this newsletter forwarded to you? Sign up to get it in your inbox.

I’ve spent the last eight years as an investor—at Andreessen Horowitz and now at my own firm, Worldbuild—watching the same pattern repeat. Software was locked in an era of homogeneity, one dictated by a well-trodden path of fundraising instead of true innovation. It was the same unit economics, same growth curves, and same path to Series C and beyond. Founders optimized for fundraising milestones instead of for building sustainable businesses, leading to companies that raised too much capital at too high valuations.

That era has ended with the advent of generative AI and the end of easy monetary policy. As an investor, I’m excited; AI has finally opened up the potential for real innovation that’s been missing since the mobile revolution. But I see founders building specialist AI products for marketing or finance as if they were building the same subscription software tools of the last decade. Those who are playing by the old framework are about to make a big mistake.

To achieve an outcome attractive enough for venture capital investors in this era (i.e., multi-billion dollar exits), founders today need to absorb Turing Award winner and reinforcement learning pioneer Richard Sutton’s bitter lesson. Sutton’s prognostication was first proven in computer vision—an early AI field in which computers were trained to interpret information from visual images—in the early 2010s when less sophisticated but higher data volume dramatically overthrew the manual programming that had dominated the field for years. Specialization eventually loses out to simpler systems with more compute and more training data. But why is this a bitter lesson? Because it requires that we admit that our intuition that specialized human knowledge is better than scale is wrong—a hard pill to swallow.

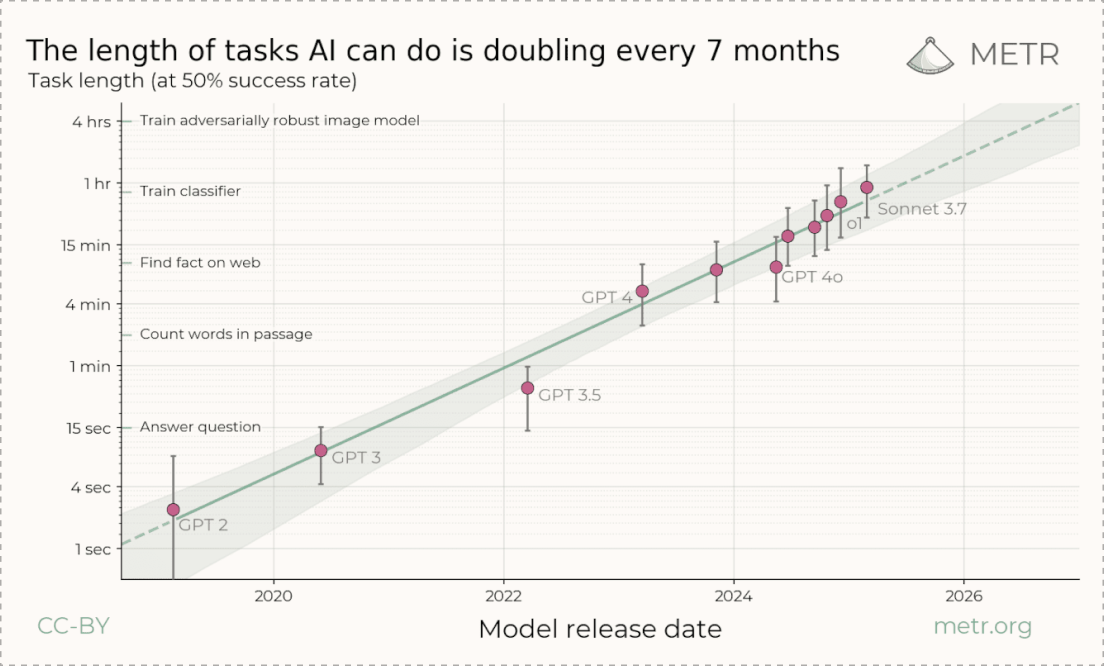

It’s already happening. It’s easy to say in hindsight that it was obvious base models would make early AI writing tools irrelevant, but this fate is coming for every specialist AI tool that bolts on AI models to some existing workflow—whether that’s in finance, legal, and even automatic code generation. Every one of these special tools believes it can create specific workflows with models to beat the base models, but the primary problem is the base models are becoming increasingly capable. The length of tasks that generalist models can achieve is doubling every seven months, as the graph below shows. Their trajectory threatens to swallow any wrapper that is built above them.

After talking to hundreds of early-stage founders building with AI, I see two paths emerging. One leads to the bitter lesson—and irrelevance in 18 months. The other leads to the defining businesses of this era. Those defining business fall into two categories: companies that build what models need to get better—compute, training data, and infrastructure—or companies that discover work that’s only possible because of AI.

Let’s dive into what each category looks like—and how to know which one you’re in.

You don’t lack ideas. You lack time.

Need more time for strategy and creativity? Optimizely Opal’s AI agent platform can free your marketing team from manual work. Automate content creation, campaign execution, personalization, and compliance. Then link your agents together into workflows that take hours off your plate. Use pre-built agents or create your own—each one learns your brand and works seamlessly with your tools.

Stop doing work that AI can do for you and get back to the work that counts.

The first path: The model economy

One way to build alongside the bitter lesson is to think about AI...

Become a paid subscriber to Every to unlock this piece and learn about:

- The four “model economy” opportunities Singh says will produce the next wave of durable AI businesses

- Why “post-skeuomorphic” apps—not AI wrappers—will survive, and the three categories where billion-dollar outcomes will emerge

- The single question every founder and investor should ask to know if their AI company is building toward relevance or obsolescence

Thanks to our Sponsor: Optimizely

You don’t lack ideas. You lack time.

Need more time for strategy and creativity? Optimizely Opal’s AI agent platform can free your marketing team from manual work. Automate content creation, campaign execution, personalization, and compliance. Then link your agents together into workflows that take hours off your plate. Use pre-built agents or create your own—each one learns your brand and works seamlessly with your tools.

Stop doing work that AI can do for you and get back to the work that counts.

The Only Subscription

You Need to

Stay at the

Edge of AI

The essential toolkit for those shaping the future

"This might be the best value you

can get from an AI subscription."

- Jay S.

Comments