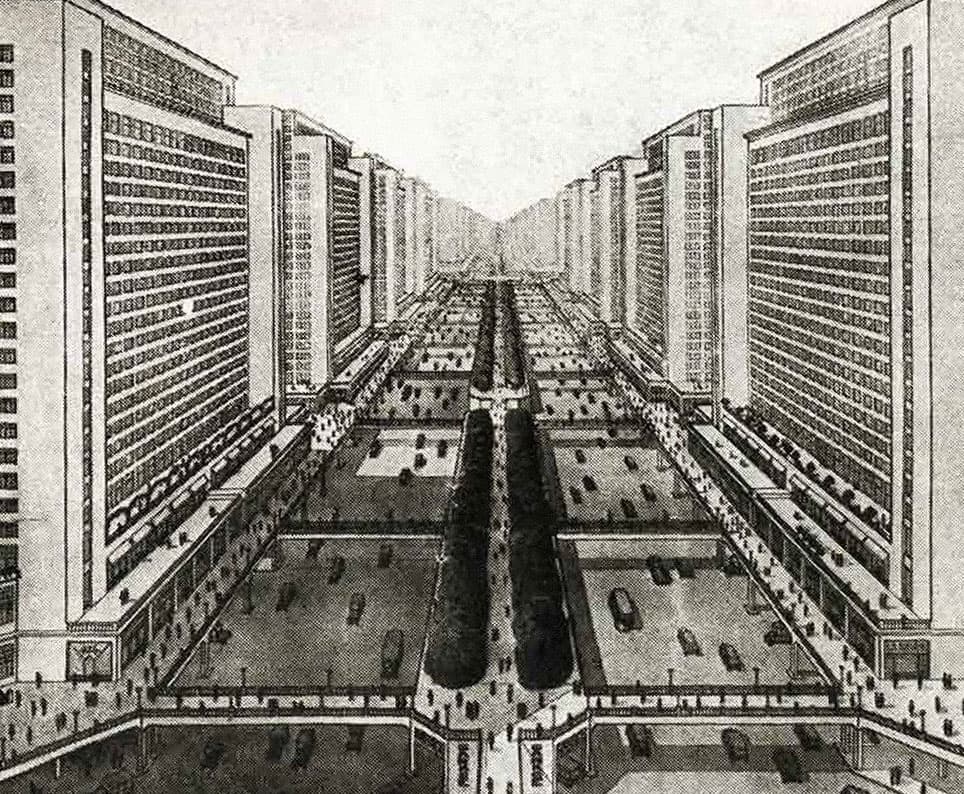

High Modernist Investors and Postmodern Investors

Hey! Nathan here. I’m thrilled to share this piece with you from behind the paywall of Byrne Hobart’s excellent newsletter, The Diff. Byrne

May 9, 2020 · 5 min readUpdated Jul 27, 2026

Hey! Nathan here.

I’m thrilled to share this piece with you from behind the paywall of Byrne Hobart’s excellent newsletter, The Diff. Byrne comes from the finance world, but is also a first-rate writer and thinker with serious range. In this piece, he uses two rival 20th century intellectual movements — the “high modernists” and “postmodernists” — to help us better understand the two main investment philosophies most traders adhere to today.

I loved it and I know you will too.

Enjoy!

Create a free account, or log in.

Every members live and work at the edge of AI. Join now.

By continuing, you agree to the Terms of Sale, Terms of Service, and Privacy Policy.

Enjoy unlimited access to all of Every.

See subscription options