The Primary Trends I’m Investing In Next Year

China, boring AI, vertical SaaS, and Apple's power

Sponsored By: Deel

Deel has simplified a world's worth of global hiring information. Our expert teams can help you navigate quick and compliant hiring in 150+ countries and so much more.

In 2003, Enron, WorldCom, and Conseco underwent the three largest bankruptcy proceedings in business history. Enron and WorldCom were brought down by accounting fraud (like the entire crypto industry); Conseco also had accounting fraud but additionally, the business sucked (again, crypto). The consensus of the market was that these assets were dead in the water.

David Tepper disagreed. The hedge fund manager purchased distressed debt from all three companies. When the companies emerged from bankruptcy, like a phoenix that dabbled in white-collar crime, his fund was up 148%—making him a billionaire.

In celebration of this ballsy trade, a former employee gifted him a pair of brass testicles. New York magazine described them as “cartoonishly huge and grotesquely veiny.” Beneath the metallic cojones a plaque was inscribed with the words “THE MOST VALUABLE SET OF ALL TIME.”

To generate outsized returns, you have to be comfortable with most people thinking you are an idiot. Prices on the assets you’re investing in will be lower and, if you’re right, the returns will be that much higher. It does, however, require a strong sense of confidence to employ this strategy. You have to be willing to be wrong, publicly, and perhaps for many years.

In the spirit of Tepper’s burnished balls, I’m forecasting what I think matters for investing in 2023. (I did this last year, and it was a popular article.) Next week we’ll examine whether my forecasts from last year were accurate.

None of this is investing advice. There is a difference between trends that matter for stocks and whether a stock is a good buy. Issues like portfolio construction and pricing matters. I’ll discuss some examples, but please do not use me as your personal Wolf of Wall Street. This is a newsletter, not Warren Buffet’s advice column.

The hardware paradigm shifts

Two forms of financial arbitrage have driven the last 20 years of the technology sector. The first was software’s superior cash flow and margin profile slowly taking over more and more economic activity. The second was outsourcing low-margin labor and hardware costs to China. Businesses like Flextronics, Selectron, Foxconn, and Pegasus built multi-billion-dollar enterprises around the idea of plucking low-skill labor from the U.S. and transporting it to China.

Ready to take the next step in your hiring journey? You’ve found the global talent but need to onboard them. Deel can help. Our expert teams can guide you to hiring quickly and compliantly in over 150 countries at your fingertips with compliant contracts, top local legal experts, global payroll solutions, and more. And that’s just the beginning. We’ve simplified a whole planet’s worth of global hiring capabilities into one platform. And it’s time you got your hands on our international compliance handbook. Inside you’ll learn about:

-Finding and attracting global talent

-Which labor laws to consider when hiring

-Processing international payroll on time

-Staying compliant with employment & tax laws abroad

In the early years of this transition, most of the outsourcing value came from labor arbitrage and tax advantages the local government was willing to give. However, as the ecosystem has developed, the value has moved far beyond mere low-skilled labor optimization. Instead, China has a robust system of suppliers, engineers, raw materials, rare earth elements, and shipping ports dedicated to manufacturing electronics. This developed into a mutually beneficial system of design in the U.S. and manufacture in China. Everyone wins—except American laborers.

However, as Chinese manufacturing skill has concentrated, so has the associated risk. Today it isn’t possible to do high-precision, high-scale electronics manufacturing anywhere else. I’ve heard anecdotes of firms being able to hire 40,000 laborers in China in the course of three days, all of whom could work on goods as complex as iPhones. You can’t get that anywhere else in the world.

This is changing—fast. China’s zero COVID policy has made work slower and more expensive than ever. It has sparked some of the most sustained political protests in years. Additional weakness in the real estate market plus an enduring economic depression mean that China isn’t the economic haven it once was. Add in the fact that, the country is committing mass genocide against an entire ethnic population, and China doesn’t look like the safe bet it once did. Apple has already made plans to move some production to India and Vietnam. Nike has tried to outsource away from China many times but mostly failed. As a result, China is facing a less performant manufacturing operation.

It will take many years to fully disentangle manufacturing from China (if it’s even possible to do so). In the meantime, I would expect that many firms will see an increase in cost of goods sold (COGS). If the scariest downside manifests itself, with China invading Taiwan, sparking World War III, there would likely be an almost complete collapse of the electronics manufacturing supply chain. The biggest risk is politically driven threats. I don’t frequently cover macro-economic factors in this publication, but the macro threat cascading through the rest of the economy is real. If I’m right, expect increases to Apple’s cost structures and other consumer electronic companies. Similarly, expect executives to examine their relationship with China to see if they can decrease their reliance. Manufacturers with specializations in India or other low-cost regions of Southeast Asia will stand to benefit.

Disclosure: I worked at Flextronics Corporate Strategy Group.

Vertical SaaS accelerates

I’ve previously defined our current period in software as the “ASS period” (After Salesforce’s Success). You take a manual workflow on a spreadsheet, automate it, stick that automated workflow onto the cloud, and profit. That simplicity feels like it’s coming to an end. Microsoft’s distribution advantages, coupled with so many of the easy opportunities already being snatched up, have made it far more difficult to build a billion-dollar horizontal software company than it was five years ago.

Perhaps the biggest disadvantage of being a horizontal platform is that you never own the key system of record for a business. When a CFO wants to cut budget, all non-essential software—i.e., all the ones who don’t own the system of record—will be the first to go. Vertical SaaS that focuses on one industry is able to own that key system and expand from there to own a merchant’s entire technology stack. Even more compelling is the opportunity for a vertical SaaS vendor to further extend to customers and suppliers. Note: Over the past nine months, I’ve done a side project with Tidemark Capital for which we’ve published more than 15 essays on this topic. I am paid for my writing.

I’m bullish on the opportunity for vertical SaaS to not only be the most important technology provider but also the most important capital partner. Fintech’s system of APIs and services is developed enough that a software platform that is sufficiently embedded with an SMB merchant should be able to replace the bank and the payment facilitator. Think of a vertical SaaS company that serves restaurants exclusively: it can offer the software that manages its food suppliers and also loans the working capital for supply purchasing.

Even better, this one-two punch of technology and capital should result in significantly reduced churn rates relative to other software providers. If we do enter into a recession, companies will aim to decrease software spend. I don’t see that happening to the same degree in vertical SaaS relative to other sectors of software, and I expect companies like Toast, Veeva, and Guidewire to do relatively well.

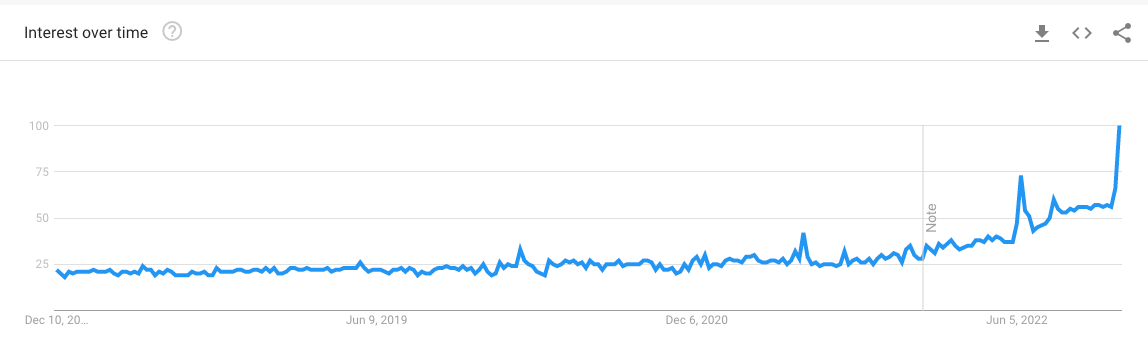

AI becomes boring again

AI search interest is at the highest it has been in five years, according to Google Trends.

I recognize that I’m part of the problem. I’ve published multiple essays over the last few months arguing that AI is one of the most important technologies in the last two decades. I still hold that view. But while adding AI significantly improves products, it does not significantly improve the outcomes for companies. There are some magic use cases where being an “AI company” will make sense, but most of the hubbub around generative AI will amount to nothing. The most interesting use case for AI is solving pre-existing problems with pre-existing solutions. As a result, AI startups will be subject to pre-existing market constraints. If you build a dating app that uses GPT3 to help men write something besides “Hey, ”that’s great—but it doesn’t solve the hardest part of building a dating app: customer acquisition. AI can make products significantly better, but I don’t see how that will negate existing market dynamics.

I’m particularly interested in companies that leverage the capabilities of generative AI without ever mentioning AI at all. TikTok, Snowflake, and Amazon are quietly doing a lot with machine learning and AI tech. As always, most profits flow to the boring use case.

Honestly, I’m not sure the best way to invest in this trend. Ideally, there would be a vehicle by which I could short a tranche of startups, but that doesn’t exist. Maybe I’ve finally found a use case for crypto? Regardless, I think the best bet is to find a company that will benefit from AI but hasn’t leveraged it yet. Once it does, its preexisting advantages should compound. There are also related potential trades with the building blocks required for AI, such as chip providers like NVIDIA or an infrastructure provider like AWS. Again, do your own research; it could be that much of this opportunity is already priced into the stock.

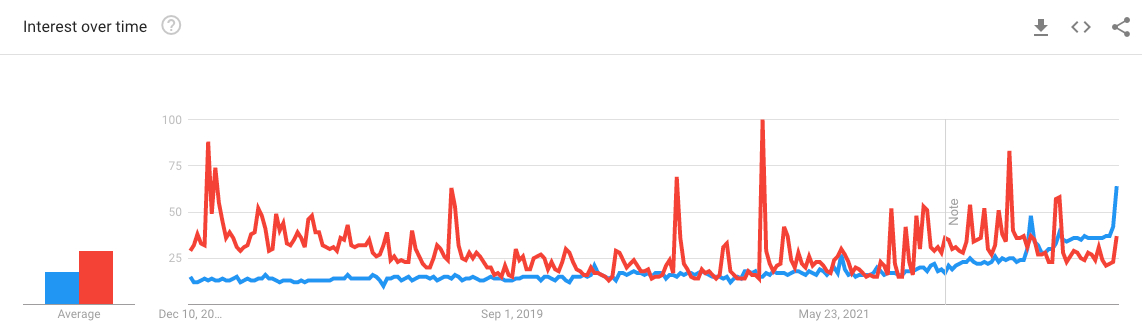

First-party ad platforms proliferate

The most important thing besides AI that happened to the technology sector in 2022 was Apple’s “App Tracking Transparency” change. These changes made it difficult for companies to track whether an ad converted someone into a paying customer. It upended the digital ad market and, via second-order effect, every business that relied on digital ads for growth.

There are probably five posts worth of analysis to be done about how this policy has affected so much of the internet—Apple is that powerful. Facebook throwing itself headfirst into VR? Apple’s fault. Snapchat’s business collapsing in on itself like a dying sun? Apple. Elon being reliant on brand advertisers for Twitter? Apple. On and on.

However, there are some winners: first-party advertisers. If you operate a website where consumers exhibit purchase behavior, you can run a relatively successful ad business. Or as Eric Suefert loves to say, “Everything’s an ad network.” This graphic from a Luma Partners's presentation starkly illustrates the situation:

While the immediate impact of ATT has been the proliferation of retail and retail-adjacent companies spinning up ad networks, it also has interesting implications for the kind of startups that get built. For a long time, there was a form of arbitrage where digitally native brands like Warby Parker or The Athletic could run a bunch of Facebook ads and acquire customers. If that doesn’t work, how will new startups acquire customers? ATT may have destroyed the advertising market but will conversely make companies turn to building out subscription products.

If I had to hazard a guess, most people are thinking they need to have an organic content play to get customers. (This guess is based on the number of people in my inbox wanting me to help them with their content.)

On the investing side, all of the companies in the above slide have new high-margin ad business lines to be built out. The financial models for all of them probably need to be adjusted accordingly. Even more interesting to watch is if any of these companies build adjacent products. Will Shopify add a consumer marketplace? Will Walmart offer software to its retail partners? ATT served as a reminder to companies that they need to build their own destinies. At any point, Apple or Google could take it all away.

The one unknown

You’ll notice that I didn’t talk about inflation. Arguably the most important story of 2023 will be if inflation gets under control, and how much interest rates need to rise to make that happen. Frankly, this is outside my publishable expertise, but this one question probably matters the most. From interest rates the rest of the economy follows.

What do you think? Am I missing anything? Where do you think I’m wrong? Feel free to email me at [email protected]. I’ll also be in San Francisco next week for an AI hackathon, so feel free to message me if you want to meet up.

Thanks to our Sponsor: Deel

Learn about staying compliant with employment & taxes abroad with Deel’s International Hiring and Compliance Guide now.

Comments

Don't have an account? Sign up!